Unity Software, new CEO to turn dominant gaming engine into profit engine

Unity Software, new CEO to turn dominant gaming engine into profit engine

Plenty of levers for this company

The CAD (computer aided design) software space has been a great place for investors over the last decades. The combination of solid top line growth and high margins resulted in compounding share prices. Barriers to entry are high, as the software tends to be pretty advanced and engineers have been trained on it for years, making switching costs.

Unity is usually not mentioned as a member of this space as it is more commonly referred to as a gaming engine. However, it is a CAD tool nonetheless as you can design the entire virtual world of your video game in this tool. You can also run simulation on the fly, i.e. playing and testing the videogame as you’re developing it. All the code that’s needed to run the game you can write within the Unity platform as well. And the engine can compile your game to run any device, from Apple iOS, to Android, Nintendo, PlayStation, Xbox, Windows, and Meta’s and Apple’s VR headsets. So Unity’s software is basically a complete production environment for video games.

Also the market positioning is good, whereas Epic Games’ Unreal engine is dominant in high-end gaming, Unity is by far the strongest player in mobile gaming development, a market which should continue to be an attractive area for investment exposure. At IPO, Unity disclosed that 53 percent of the top 1,000 games in Apple App Store and Google Play were built on their engine, with 93 of the top 100 game development studios being customers. The company also highlighted some high profile titles which were developed on the Unity engine, such as Tencent flagship titles ‘Arena of Valor’ and ‘Honor of Kings’, as well as the popular ‘Pokemon Go’ from Niantic and Nintendo — pokemon are everywhere apparently:

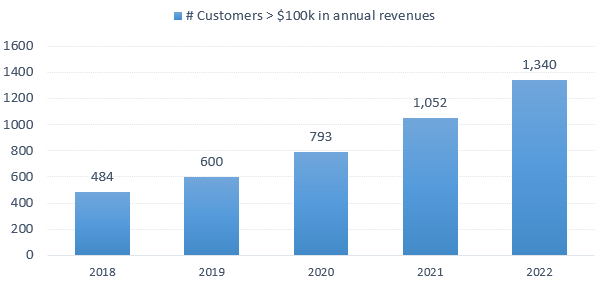

Overall, Unity has over 1,300 organizations generating over $100,000 in annual revenues as customers:

Also designed art and other models from popular CAD tools — such as those from Autodesk — can be easily imported into Unity’s engine. This makes it possible to do advanced design in specialized tools, and use them afterwards in your game via Unity’s engine.

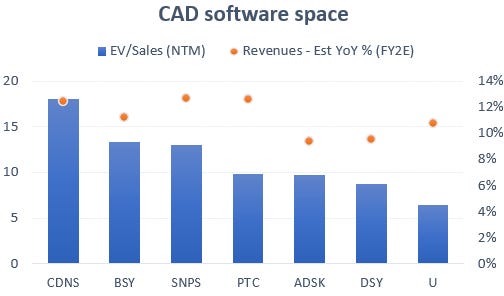

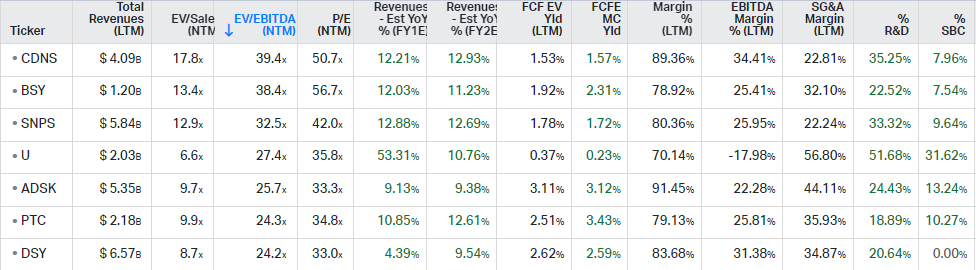

When comparing Unity to the CAD space, the stock trades on a strong discount, although that isn’t due to a lack of growth. You can see that Unity is expected to generate double-digit top line growth rates, similar to other CAD names:

By far the biggest reason for this discount is that the previous CEO John Riccitiello made a number of questionable decisions which we’ll get into. Riccitiello has a very mixed track-record to say the least, but he’s gone now and replaced with Jim Whitehurst, who built Red Hat into a fantastic machine and subsequently sold it to IBM at a high price tag. But first, let’s have a better look at the product..

Unity’s developer conference

Unity held its developer conference in November of last year, which was quite impressive. The company showcased the latest upgrade of its software, Unity 6, and all of the accompanying performance improvements. These were showcased in the Unity engine and a series of virtual worlds they had built with it, one of which I’ve linked here. Unity 6 will also allow more games to be played inside of a browser, making gaming even more accessible.

An example of how you can develop a gaming world in the Unity editor is illustrated below. You can design each object, assign physics to it how it should behave — e.g. this object should float in the air and the other should fall to the ground — as well as write code for each element. You can code both in C# and Javascript in Unity, so that’s good news as I’m a bit of a Javascript fan.

It has become clear that LLMs can massively speed up game development and Unity has been putting a lot of effort into this. You can use the built-in AI models to get instructions on how to implement your ideas in the software. The LLMs can obviously write code, and they can also design objects and worlds for your game. You could even describe how characters should behave and the AI will generate a behavioral tree for each character in the editor, which you can then adapt.

You could also insert an externally trained AI model within your videogame, for example, so that the AI can play as your adversary, or take on the role of characters within your game. So that you can conversate with them like you would with ChatGPT, giving a totally unique user experience. These LLMs run on your local device’s compute, so that should be good news for the demand for neural processing units (NPUs) within CPUs. Companies such as Arm, Qualcomm, Intel, AMD, and TSMC have all been talking up these opportunities in recent months.

Here’s Unity’s previous CEO discussing how their AI can generate virtual objects and worlds, saving creators a lot of time:

“And what will you do if you want an environment with a river, maybe a stream coming off the side of it, a mountain, clouds, et cetera? That could take somebody weeks, if not months, to create in a real-time 3D digital asset collection. Guess what? You can use the words I just used to describe that, and it will show up, this is hugely valuable to them.”

He also explained how the co-pilot should expand usage of the engine:

“We get several thousand people per day that download Unity, they look at the editor and say ‘wow, this looks like a 747 control panel’, it is complicated. Where they need art assets, or lighting assets, or other things to advance into the game or scripts, they can just ask for them. It radically will simplify and bring new users onto the platform. Over time, we’ll capture a much larger portion of the people that hit the top of the funnel for us and begin their journey on real-time 3D creation.”

Once these AI models are in their release version — they are currently still in beta — pricing will be based both on monthly subscriptions and used compute. So the increased usage of generative AI within games development should become a tailwind for Unity in the coming years. This opportunity is somehwat similar to what we discussed for Cadence and Synopsys in advanced semi design.

The mobile gaming market

The mobile gaming market should remain an attractive area for investors. It is a $90 billion market expected to grow at a 7% annual rate (chart below). This market was strongly impacted in ‘22 by Apple’s ATT (app tracking transparency) policy, requiring apps to request permission from users before tracking their data across apps or websites.

Traditionally, users could be automatically tracked via an anonymous device identifier, giving advertisers insights into the interests of a user. As most iPhone users subsequently opted out, this brought a large correction in the value of the mobile ad market during ‘22, as well as with covid lockdown policies unwinding.

However, this damage is now done and we should continue to move forward from here. And even though Google will phase out cookies in the coming years to replace them with a fully anonymous profile — a vector indicating the set of interests of any user — as Google makes almost all its money from ads, one can be reasonably sure that this won’t work any worse than the cookie mechanism, and possibly even better. Although they’ll likely use these changes to try moving volumes away from competing ad exchanges and supply and demand side platforms to further expand Google’s dominant position in online ads. This is a potential topic for a future article.

The mobile gaming market is really divided into two parts, one is in-app purchases, which is around 80% of the market, and the other is advertising, which is used mostly in casual games where puzzles are a big category i.e. things like Candy Crush. It’s actually the in-app purchasing market which got hit hardest by Apple’s changes as it became much harder to target new players who spend money in games. That being said, the damage should be done, companies have been adapting to Apple’s changes, and the mobile gaming market should be able to move forward from here.

Unity’s new pricing model

Competitor Unreal has a smart pricing model where they charge 5% on a game’s revenues above $1 million, thereby opening up their editor freely to new and small users, while monetizing those who are making substantial revenues in the gaming business. Additionally, they offer an enterprise version of their editor which includes customer support and more advanced features, and which is a priced based on a monthly subscription per seat.

Unity on the other hand only had this classic, per seat subscription model depending on the version of the editor you’re using. So the hobbyist version comes for free, Pro is around EUR 1,900 per year, and Industry comes at around EUR 4,500 per year.

Previous CEO Riccitiello rightly identified that they needed to move to a pricing model similar to the Unreal Engine, however, he tried to implement this retroactively i.e. on games already in circulation. So that’s sort of going back to your customers and trying to charge more for purchases already made. This obviously drew a lot of pushback from the developer community and Unity was at the center of the gaming media’s attention for some weeks.

So the new pricing model they’ve now announced is that in addition to the subscription per seat, studios will also have to pay the lesser of the following two. One, 2.5% of revenues above $1 million, or two, a fee based on the number of installs during the first month of the game. I’m not sure why they made it overly complicated with a dual pricing structure, but anyways, a gaming studio can pay the lesser of these two calculations.

Below I do some back-of-the-envelope modelling on how this new pricing model can lift earnings in the medium term. The mobile gaming market will grow to around $100 billion in size in the coming years and I’ve assumed a share for the Unity engine of around 55%. I’m modelling in 0% for the console market, so everything they will get from this market is pure upside. I’m assuming that both pricing formulas should give similar results on average, resulting in an average take rate of 2.5%. Basically all of these revenues will fall through to the bottom line, but the payments processor will take a cut and Unity will also need a team to monitor whether the gaming studios are being honest, so I’ve assumed a 90% operating margin. This would lift EPS with close to $3 over time, and putting the combined EPS on a 30x multiple, which is a low multiple in the CAD space, this would already lift the share price with 270%. If this could be achieved over a 3 year period, this would give a 55% IRR (annual return).

Games regularly have to be updated with new levels, new characters and new items, so while a three year timespan might be a bit optimistic of moving games over to Unity’s new engine and pricing model, this analysis shows that over time the new pricing model should make a very substantial impact on the business.

So there is good potential from this measure alone. I haven’t modelled in any real share losses as competitors such as Unreal Engine and Cryengine charge a 5% royalty fee, so I think something around 2.5% sounds very reasonable, and I suspect that most studios will be understanding that Unity needs to be able to start generating profits as well. Additionally, Apple and Google remain the two big revenue drains for app developers really, as they charge around 15 to 30% of revenues. This is exactly the reason Epic Games has been taking them to court.

There a number of open-source engines that developers could shift to, however, these won’t have the quality level of Unity. And for small indie developers, Unity will remain free, so there isn’t really a reason to make the move for these either, and they can still help in generating a network effect around the software by making tutorials, participating in forums etcetera. All the tutorials in mobile games development I’ve seen are based on Unity, making it for newcomers the tool to learn.

The other form of competition for Unity is the in-house market, large gaming studios can build their own engines to develop games. Examples here include EA, Bethesda, Ubisoft, Rockstar, and of course Nintendo. However, these engines are oriented towards developing high-end PC and console titles, and this is the reason why Unity is so dominant in mobile. It could be possible that the very large studios decide to build their own engine for mobile games development, however, given that I’m modelling in above that 0% of new revenues will come from the console market, I think that the modelling should be sufficiently conservative to factor in some possible market share losses in mobile. It is also possible that the new AI models Unity has been training will provide a compelling feature to keep using their engine.

Lastly, Unity disclosed that not a single customer is contributing more than 10% of revenues, so customer concentration isn’t overly high. And above, we already saw that its overall customer base has only been widening. So overall, I’m not expecting any large market share shifts away from the Unity engine.

Apple Vision Pro as a new revenue driver?

I haven’t been really excited about VR so far but it does look like Apple could successfully start expanding this market over time. Vision Pro will be the first release in a series of headsets, and as the technology improves over time, this will allow cheaper versions to become available and expand the market. Note that the current name already includes the word ‘Pro’, so presumably at some stage we should get the regular Apple Vision. Long term, this should be interesting for Unity as the company has a 65% market share in VR games.

There is also a substantial non-gaming opportunity in virtual training. Volkswagen uses Unity’s tech to its train workers as an example. But one can imagine not only the training of skilled workforce and engineers, but also sales people practicing in virtual client environments, or perhaps doctors practicing surgeries.

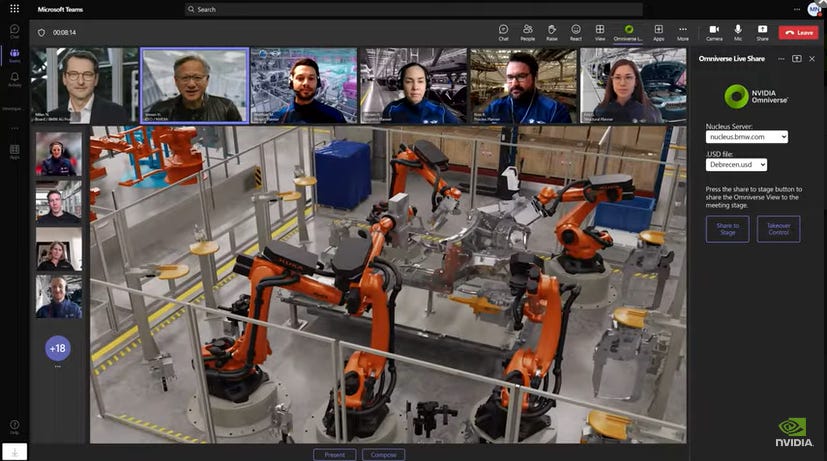

Unity is also bullish on the opportunity in digital twins, i.e. having 3D virtual environments of real world assets such as factories, ports, and cities. With cameras and sensors you can then feed live real world data into the software, providing analytics and detecting problems early on. Most of the CAD players are looking at this opportunity, from Dassault to Hexagon, but also Nvidia has launched a nice digital twins product which BMW has been using to plan and monitor their factories.

In AI, Unity has been leveraged to train robots in virtual worlds, this is done with reinforcement training, which was the hottest area in AI just a few years ago. Such as when AlphaGo beat the world champion, Lee Sedol, and when AlphaFold subsequently managed to learn how to fold proteins from the basic mRNA code, something which before would have required an entire PhD thesis for a single protein. Thanks to reinforcement learning, researchers can now use AlphaFold to quickly get an idea what shape proteins will have in 3D. Currently all the attention has shifted to LLMs, however, I expect reinforcement learning to remain a vibrant area within AI, especially in the fields of robotics and task learning.

Overall, Unity disclosed on a recent call that these industry opportunities are contributing 30% to the engine’s revenues. And here’s the previous CEO giving some more details:

“We generate revenue in digital twins from three activities. We generate from professional services that enable a customer to get that real-time digital twin up and running. And this can be for an airport, a city, a manufacturing facility for high-end watches or automotive, or a retailer. And we’re seeing strong demand from all of the sectors I just mentioned.

The second component is the seats that they consume. And originally, they consumed the same that a game developer would use. But what we’ve done with our industry SKU is to provide tools that they would need for their specialized use cases. So that’s why it’s a premium SKU with added value to it.

The third, and this is really more nascent, is ratable revenues once they’ve got their digital twin up and running, where they’re using us for simulation, rendering, computer vision, and this is essentially a cloud model.

Where we are right now is a situation where our largest revenue stream is professional services, our next largest revenue stream is seats, and our third and more nascent stream is ratable. The reason that we brought partners like Capgemini and Booz to our own professional services business, is that our own capacity on that front is something that we did not want to increase. In fact, we might want to decrease it a little bit. And once the model is proven to partner with third-party systems integrators, to scale more rapidly. That would result in less professional services revenues, more seats, and more ratable revenue streams. So we’ve been transforming our business model perspective sort of under the covers to make sure that we’re scaling.

Now in terms of demand, frankly, we’ve been supply constrained, not pushing a lot for demand. There’s a lot of interest in government, manufacturing — particularly the automotive industry — but also specialty manufacturers. There’s a fair amount of interest on the retail side, and there’s a lot on architecture, engineering and construction.

What we’re working to do between now and the end of the year is to bring it down more to a handful of turnkey solutions that we can scale rapidly. We think that’s the best way to scale this business into a very high-margin contributor to Unity because it leads to the two high-margin businesses we like, which is SaaS and consumption revenues. So that’s the evolution.”

So basically they’re trying to move away from lower margin and competitive services revenues to high-margin software revenues, and then work out vertical solutions which can scale rapidly. Long term, there certainly could be an opportunity here.

The CEO change — Riccitiello out, Whitehurst in

As already mentioned, why Unity is trading at a discount has to do with the missteps Riccitiello made. Besides the new pricing model debacle, he also pursued numerous acquisitions, a strategy similar to the one he undertook during his time as CEO of Electronic Arts (EA) and which also led to poor outcomes there. Barron’s explains:

“Riccitiello made numerous deals during his tenure at EA that didn’t work out. EA’s stock also fell by more than 60% during his time as CEO. One of Riccitiello’s first moves at EA was to buy a $167 million stake in Chinese online game operator The 9 Ltd (NCTY). The company’s share price fell by more than 90% in the ensuing years. Riccitiello also made the expensive decision to compete in the online subscription multiplayer market against World of Warcraft, which fizzled. He also acquired numerous gaming studios — including Playfish, PopCap, and Pandemic — all of which were at least partially shut down years later by EA. In November, Unity announced a $1.6 billion acquisition of Peter Jackson’s movie visual effects company Weta Digital. At the time, Unity executives declined to give historical revenue, but gushed about the potential market opportunities far off into the future. So far, Unity has offered little evidence to show that the Weta deal is paying off, so it isn’t a surprise that investors are skeptical about Unity’s latest billion-dollar-plus deal and whether it can properly integrate the companies.”

There were two reasons for the Weta acquisition. Firstly, to further build out the visual effects tools which Peter Jackson had developed and market them to a wider audience. Secondly, to grow these design tools in the gaming world. Although you can do your full game design in Unity, the larger game studios will have specialized tools for the artists while the coders develop the game in the Unity engine. As there can be multiple artists for every coder, this is obviously an interesting market.

So I can see the logic here, although I would have preferred to first focus on building out a proper monetization model for the gaming engine. This would allow the stock to trade on a higher multiple, and subsequently Unity could have leveraged this higher valuation to build out their software portfolio.

Returning focus to the core Unity engine is the strategy which new CEO Whitehurst is implementing. Jim Whitehurst is actually the interim CEO but his track record is really good, and having him seen present at the recent conference, it seems quite likely that he will be tapped to continue in this role. He certainly made the impression that he was in it for the long haul.

During Whitehurst’s time at Delta Airlines, he oversaw the company’s recovery from bankruptcy. Subsequently he made the move to Red Hat, a relatively niche Linux distributor which he grew into a major player in open-source enterprise software, and which was successfully sold to IBM for $34 billion. And now his first focus at Unity, is to turn this well-positioned software asset into a high margin machine.

His plan so far is twofold. First, monetize better the value of the engine as discussed above. Second, cut costs by focusing on the core business. In early January, Unity announced that it will be laying off 25% of its workforce, or 1,800 jobs. We’ll have a look below at how these should affect the share price. In the meanwhile, here’s Whitehurst discussing the restructuring plan on his first call in November:

“As we get into next year, more focused execution generally leads to success in the marketplace. And so I’m thinking of ‘24 already, you’ll see kind of improved gross performance. The good news in the things that we’re looking at, it’s not like we’re peeling off businesses that are highly EBITDA positive because they don’t fit, right? In a good way, we’re investing in a lot of things. And so this is more about looking at kind of peeling off some things that we were doing that frankly aren’t profitable. The key is making sure that we build a pathway to profitable growth.”

The IronSource acquisition

Unity’s previous CEO made the IronSource acquisition in ‘22. Now, this isn’t a bad business, it’s the key competitor of Applovin which we discussed previously, and there is rationale to this deal.

IronSource basically has three key businesses. Firstly, there’s the mediation platform, which allows a game publisher to connect to a wide variety of ad networks and exchanges, ensuring that its ad inventory can be sold to the highest bidder. This is a typical take rate business, where IronSource’s platform will charge around 20% of revenues generated. Secondly, there’s a discovery product, where you can advertise your app within other apps. IronSource will charge you per 1,000 installs, so they need to make sure they can deliver those 1,000 installs for you at a cost lower than you’re buying them at. So this part isn’t really a quality business, it reminds me of Criteo, but they do have a lot of data on which gamers are playing which types of games. So for their competitor Applovin this has actually been a well performing business. Lastly, there is a subscription business that provides all sorts of analytics and recommendations to grow your apps.

The rationale here for doing this deal is that Applovin is the dominant player in the ad mediation / discovery market, generating around $3 billion in revenues and $900 million in GAAP EBITDA over the last twelve months. This compared to Unity doing around $1 billion in revenues and still running GAAP EBITDA losses. So if they could leverage Unity’s dominant position in mobile gaming development, and then cross-sell IronSource’s platform to Unity’s user base, there is a large opportunity. Unity could also dangle an attractive carrot by giving discounts on their engine, if users in return make the switch to IronSource from Applovin.

The other attraction is that you could provide the industry with a more integrated software product, supplying the entire value chain for gaming studios, from development and publishing, to monetization and user acquisition.

I don’t dislike this idea and I suspect that if this works out and the now combined company turns into a highly profitable cash generator, quality-growth type investors will be interested in Unity’s strengths and dominant positioning along the entire mobile gaming value chain.

Here’s Unity’s previous CEO discussing the logic for this deal:

“Our combined company will enjoy a roughly 50-50 revenue mix between our creation and growth technologies. The traditional model employed by most game companies are separated big silos: you build your game, then there’s a pre-launch testing phase, and then the focus is on marketing and user acquisition. At Unity, we were in the early stages of the industry’s business model, but we are going after the biggest prize, a unified creation and growth platform.

There’s a reason the game industry is considered hit driven. Hits consume a huge portion of the industry revenue and they’re hard to predict, especially with new IPs. Integrating the creation and growth sides of the business under one platform, where a developer can test a level, a whole game, or a version with different features with real consumers, this is a huge step towards turning the guesswork to adding a big share of science.

Once closed, Unity shareholders will own approximately 74% of the new company and IronSource shareholders will own the balance 26%.”

Unity was already running a business somewhat similar to IronSource pre-acquisition, which was roughly making up 50% of its revenues. So effectively they are consolidating this space to become a more effective competitor to Applovin. In their prospectus, the company highlighted the following high-profile clients of this business:

Interim CEO Whitehurst gave a brief update on the integration:

“We’ve made progress in integrating IronSource, but a lot of that is getting the core stuff together. Now getting the flywheel that we think we can do, of the real synergies between the editor and grow businesses, is something we are just getting kicked off.”

Financials — share price of $35 at time writing, ticker U on the NYSE

On the sell side’s modelling, the company can move to a 4 to 5% FCF yield in the coming years which is attractive, however, stock based compensation (SBC) is still high at $640 million over the last twelve months. Over time, FCF generation should become fully sufficient to offset SBC dilution with buybacks. And also the workforce reductions should help bring SBC down.

In recent quarters, Unity has been mentioning that the Chinese gaming market has been forming a headwind. However, recent news reports are claiming that the regulatory tightening has now come to a halt, as the Chinese government wants to stimulate sufficient economic growth and attract foreign capital. So the CCP should now start taking a more dovish stance towards the internet giants, thereby also limiting further restrictions on gaming.

As Unity is laying off 25% of its staff and with the company expected to have non-GAAP operational costs of $1.35 billion for this year, if these could be lowered with 25%, that alone would nearly double current adjusted EBITDA numbers. This would bring the EV / EBITDA multiple below 21x, which is attractive compared to a peer group trading around 31x on average:

So, these cost cuts could lift the share price with around 25 to 50% assuming an EV / EBITDA multiple of 25 to 30x, which is still somewhat below its peer group.

Overall, we have a new CEO and one with a good track record, who seems motivated to turn this into a successful business like he did with Red Hat. I think it is likely that the board will offer him a permanent CEO role at the company. And over time, we should get a leaner organization and with a much better monetization model to drive revenue growth for the company.

As already mentioned, the new pricing model could quintuple earnings over time. Additionally, shareholders get the upside if the new digital twins product grows into a success, and as game developers start using generative AI increasingly in their workflows. Finally, if you see loads of people buying Apple Vision Pros over time, Unity should be a long term winner from this.

And as the core business is a high quality software asset exposed to the attractive growth in both mobile and VR gaming, I suspect that the market will value this at an attractive CAD software-like multiple over time.

If you enjoy research like this, hit the like and restack buttons, and subscribe if you haven’t done so yet. Also, please share a link to this post on social media or with others who might be interested, it will help the publication to grow.

I’m also regularly discussing tech and investments on my Twitter.

And I’d also like to give a shout-out here to our friends at

, a great substack looking at quality compounders. They recently did research pieces on Eagle Materials and Novo Nordisk as just two examples.Disclaimer - This article is not a recommendation to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it can not be guaranteed that all information used is of this nature. The views expressed in this article may change over time without giving notice. The future performance of the mentioned securities remains uncertain, with both upside as well as downside scenarios possible.