Synopsys + Ansys, a semiconductor software powerhouse

Synopsys + Ansys, a semiconductor software powerhouse

An overview of the deal

Ansys' strengths in semiconductor simulation

Ansys has a variety of software simulation tools used in the design of semiconductors with its RedHawk platform now integrating most of these. Semiconductor design utilizes a chain of software tools, each focused on a particular task. The three companies that dominate this industry are Cadence, Synopsys and Mentor Graphics (Siemens), while Ansys is the strong player in the overall simulation market. Around 30% of Ansys’ revenues are now coming from the semiconductor end-market (chart below), while the company’s other two large revenue exposures, and more traditional end-markets, are aerospace & defense and automotive:

Ansys is widely known for its physics-based simulation tools, such as fluid dynamics and structural analysis. The company has much more capabilities than the three shown below, but it should give a feel of what their software can do.

These tools are used by PhDs and advanced engineers, both of which have been trained for years on the tools, making revenues extremely sticky.

The company’s CEO explaining the business of simulation at the Barclays conference:

“So Ansys is an engineering simulation software company. And what that means is we build software that allows our customers to be able to analyze and evaluate the behavior of a physical product, completely in the virtual domain. Using our technology, our customers can visualize the behavior, the failure potentials, the response of any product that they’re trying to design completely in the computer without the need for physical prototype and without need for experimentation. The way we do this is our software really encompasses the basics and the fundamentals of mathematics, of physics, of computer science.

It’s the accuracy of the simulation that is really important because you’re using simulation as a way of evaluating a physical phenomenon. And you have two possibilities. You can rely on a physical experimentation, i.e. you could build a prototype and then physically evaluate it in the lab. So if you were testing the safety of a car, you could build a model of the car and you could slam it against the wall at 30 miles an hour, and that will give you some perspective. Or you could do that in software. The price differential is significant. Building a physical prototype in advance of the production model of a car can be quite expensive. And then slamming it into the wall requires a significant amount of instrumentation. That’s very expensive, maybe $1 million to do a single crash test. And that gives you one scenario, a head-on collision at 30 miles an hour for example. But if you could do that in software, you can do that with significantly less cost. You can run multiple experimentations and you can do so really early in the design process before you lockdown any of the decisions. So there’s real advantage to doing it in software, but it only works if the software is accurate and we certainly pride ourselves at being very accurate across our simulation capabilities.

The other thing that I’m really proud about is the completeness of the portfolio. The problems that our customers are dealing with are not tied to a single individual physics. These are not uniquely structural, fluid dynamics or electromagnetics problems. This is really the integration of all of these, that’s what we refer to as multi-physics problems. So if you take the example of a car crash, you might imagine that it is a structural analysis i.e. you’re trying to analyze the physical integrity of the car to see if the driver would be safe. But the reality is it’s a multi-physics analysis because you’re simultaneously analyzing the deployment of the airbag and that’s a fluid dynamics problem.

We’ve got representation across structures, fluids and electromagnetics in the semiconductor space; also optics, safety analysis, embedded software and I could go on.

We moved our portfolio from being tool-oriented towards more of a platform-oriented view. So while we have a lot of simulation capabilities as individual tools and customers can use them, we have also integrated this together as part of a platform. So that evolution has put us in a very strong position to deal with these emerging use cases that customers have.

If you look at aerospace, the trends there are towards sustainability. So moving away from traditional fuel to sustainable fuels, electrification, hydrogen, thinking about VTOL aircraft. They’re making design decisions now that are going to stay with them for the next 25 years. And to facilitate this transformation requires multi-physics analysis.”

Ansys is the top player in the simulation space, with an estimated market share of above 25%. Competitors include Altair Engineering, but also the CAD software providers such as Dassault Systemes, Autodesk, Siemens, Cadence and Synopsys among others. Designed models can be uploaded from the CAD software into Ansys’ tools, to analyze and simulate them under a variety of physical conditions.

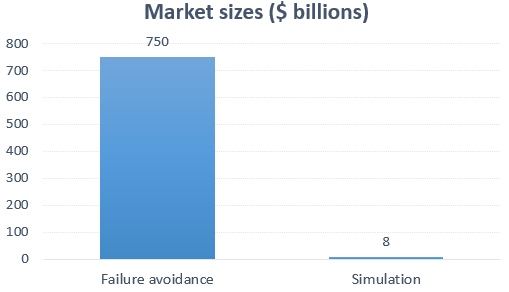

According to Ansys, the global annual market for product failure avoidance is $750 billion, while $8 billion is spend on simulation. Obviously not all product tests can be digitally simulated, but it does suggest large room for growth, especially as the physical world can get better modelled in the digital world over time. In the future, it is conceivable that at some stage we’ll have good digital models of a human cell and the human body as a whole, which would allow new drug molecules to be initially tested digitally.

Another reason for this low penetration of simulation tools in the failure avoidance market is that Ansys’ software is typically used by PhDs and other advanced engineers, but the company has been working on making their tools more user-friendly so that they can be used by a wider range of people. Ansys’ CEO discussed at the JP Morgan conference for example how they’ve been integrating their simulation engines into software from other providers:

“At our last investor day, we talked about how there’s a company that’s providing software to eye surgeons. And under the covers, unbeknown to the physician because the physician really has no interest in learning how to use simulation software, the technology is taking advantage of simulation and presenting the results to the surgeon. So the what-if analysis that the surgeon would normally go through based on their experience, they can actually use physics-based analysis to drive them towards the best surgical outcome. That’s an example of a next-generation use case where simulation is embedded, and that goes well beyond anything that we have done in the past.”

The CFO continued:

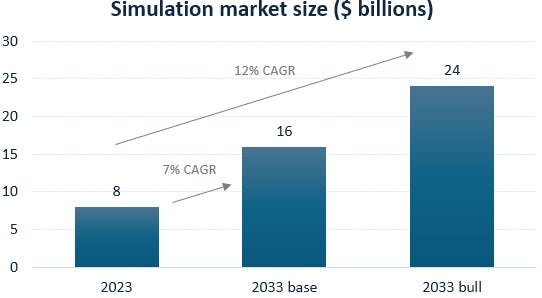

“If you’d like to see the data, the core simulation market is about $8 billion, and our estimates are that over the next 10 years, that core market could roughly double. The emerging use cases that Ajei just referred to in terms of contextually embedding simulation for non-experts, our estimations are that if that would continue to progress over the next decade, that doubling could nearly triple.”

So the company is guiding here that their market could double to nearly triple over the next decade:

One really interesting feature of Ansys’ business model is that revenues not only grow with the number of software seats and modules being sold, but also how much computation the clients’ workloads need. This is very similar to Synopsys and Cadence, where they are working out new pricing models as their CAD software is being used for compute intensive AI workloads, such as generative AI in semi design.

Ansys’ CEO detailing their business model and the computational nature of their software:

“In our case with simulation, a single engineer could kick off a job that could run for across thousands of cores and for days or weeks at a time because you’re solving these incredibly large problems. And a single engineer could kick off a number of different jobs. So many of our customers have invested in datacenter technology to try to build out compute capability. And in fact, this is a dimension of growth for us, which separates us from traditional enterprise companies because when they sell software, they can grow by selling to more users or more products. We can sell more users and more products, but we can also sell more computation. We sell a license to be able to use our software across more hardware, so that’s a really interesting avenue of growth. With our cloud strategy, we also support them to use our technology in the cloud for scale-out compute. We work with Microsoft Azure and Amazon AWS.”

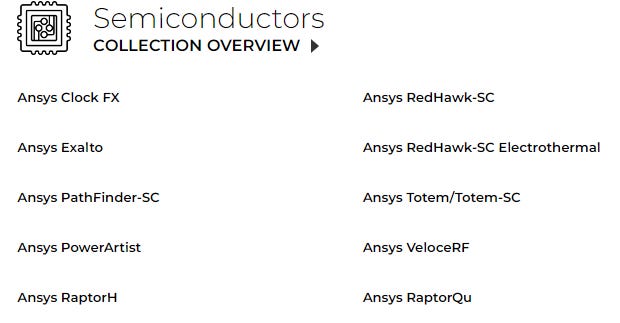

During the 2000s, Ansys acquired a range of software tools focused on semiconductor simulation, below we’ll go through the most important ones.

PathFinder simulates the effects of electrostatic discharge (ESD) on a designed IC (integrated circuit). ESD occurs when there is a sudden buildup and release of static electricity, which can damage and destroy electronic components. PathFinder analyzes the physical layout of an IC and its underlying circuitry to identify potential weaknesses. The software can simulate different types of ESD events to help designers understand how their designed ICs will perform under real-world conditions. The software can help in optimizing the placement and sizing of ESD protection devices, improving the robustness of the IC. The software is both available in the cloud and on-premise.

RaptorH is an electromagnetic (EM) simulation software for ICs. Early analysis helps pinpoint issues, minimizing later debugging and accelerating overall development. The company has a similar software for analyzing superconductive processors called RaptorQu, enabling the design of tens to hundreds of qubits (the ‘transistor’ in a quantum processor which can have four states).

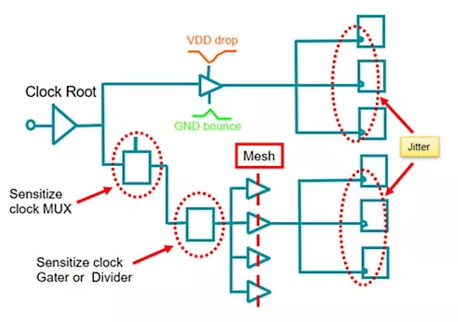

Clock FX simulates all clock paths in an IC design and identifies contributors to jitter. The clock path is the network of wires and buffers that distributes the clock signal throughout a chip, and must reach all parts of the chip with minimal delay and skew.

Most of these tools have now been integrated into the RedHawk multi-physics platform, which can also analyze voltage drop, electromigration, heat dissipation and signal integrity for chips, multi-die packages, interconnects, and printed circuit boards (PCBs). The platform is also delivered over the cloud.

A detailed thermal analysis of a PCB with RedHawk — pretty cool software:

Ansys’ CEO discussed the trends in semiconductor simulation:

“When you’re considering a traditional system on chip (SoC) and IC analysis, you use your more traditional tools. But the moment you’re now considering a 3D-IC structure, you have to worry about the integration and the interaction between the different layers. So you’re thinking about electromagnetic interference, signal integrity, and other kinds of analysis. And that requires physics-based analysis, which is where we come in. We have customers like Nvidia for example, they’re taking advantage of our technologies to pursue the physical design limits as they start to use RedHawk, Raptor, all of our products to improve their design.”

An example of a 3D-IC with HBM DRAM dies stacked on top of a base die, connected by through-silicon-vias (TSVs). These are the types of modules you can create with the latest advanced packaging techniques such as SOIC and CoWoS.

- TSMC - WikiChip")

This semiconductor software portfolio has been built up both by acquisition and internal R&D, Ansys’ CEO detailed their strategy here:

“Ansys started of as a structures company, and for many years was essentially growing organically. If you look at our expansion into the second major physics area which was fluids, it was driven by two acquisitions, one in 2002 and one in 2004. Then subsequently, we’ve done over a dozen acquisitions in the fluids space. It’s been a combination of both organic investment as well as inorganic activity. So that’s a great example where we’ve got really good capability, electronics as well.

What I would point to recently is optics. A few years ago, we didn’t really have an optics presence, and we identified autonomy as an area where there was going to be growth, and we didn’t have support for camera and lidar. And so we looked around for an appropriate partner and then eventually decided to acquire a company called Optis. This was in 2018 and that obviously went well. And then from there, we used that as an anchor to build out a couple of other optics capabilities. We acquired a company called Lumerical which gave us photonics capabilities, and we acquired Zemax which gave us lens design.

But more than just simply the acquisitions, we’ve organically invested in them and integrated them together to have an integrated optics offering, and that’s typically what we do. It’s not just simply a matter of doing an acquisition and letting it live separately from the rest of the business. It’s doing acquisitions, integrating them together because ultimately, customers are not looking for point solutions. They’re looking for an integrated offering across multiple physics, and that’s what we try to do with our offering.”

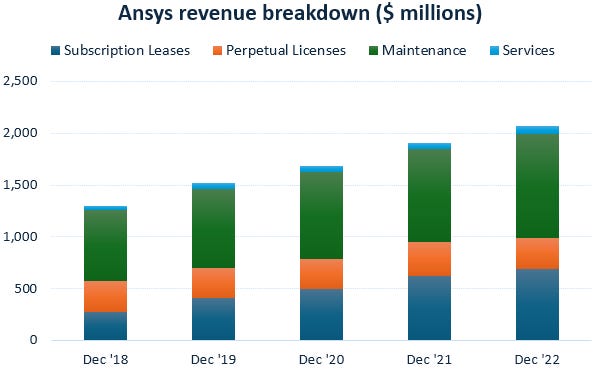

The company’s revenue breakdown shows how revenues are now largely recurring, i.e. flowing from subscription leases and maintenance fees. Old-style, one-off perpetual licenses are only 15% of revenues now and have been declining in the mix — I suspect Synopsys will try to move away from this business model entirely, transitioning customers to more attractive, annually recurring subscriptions.

Ansys makes attractive gross margins of above 90%:

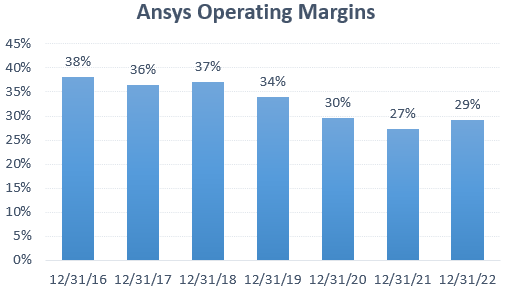

However, operating margins have been sliding:

Ansys’ CFO discussing the outlook for their operating margins at JP Morgan:

“We were kind of in the low to mid-single-digit growing category with very high margins, and the intention was to make deliberate investments to accelerate growth. So if you look back 5 years up until about 2021, you would have seen that margin investment in the business. And if you look at our outlook, the guidance that we gave at our investor day was that we see significant operating leverage in the business through our cumulative unlevered operating cash flow guidance of $3 billion from 2022 to 2025, that compares to approximately $2 billion over a comparable period prior. Underwriting that is the 12% CAGR of ACV (annual contract value) growth that we guided to over that time period and operating expenses growing at a relatively slower pace than that ACV.”

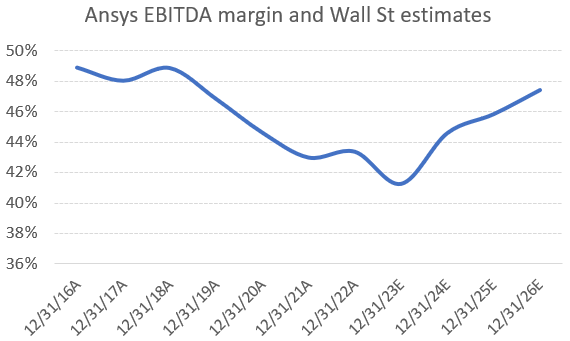

If investment can now gradually be reduced relative to top line growth, this will allow for margin expansion going forward. Wall Street does look very bullish on this story:

A brief overview of Synopsys & the potential roadblocks to deal approval

Synopsys is one of the two leaders in EDA (electronic design automation, also called ECAD), these are the software tools used to design the chip layout. I went in detail over this business here, and liked especially the increasing role of AI to take over workloads, which should allow the EDA providers to grow in importance within the R&D budgets of the semiconductor designers such Nvidia, Qualcomm, and Broadcom.

The EDA industry is highly consolidated with three companies largely controlling the landscape:

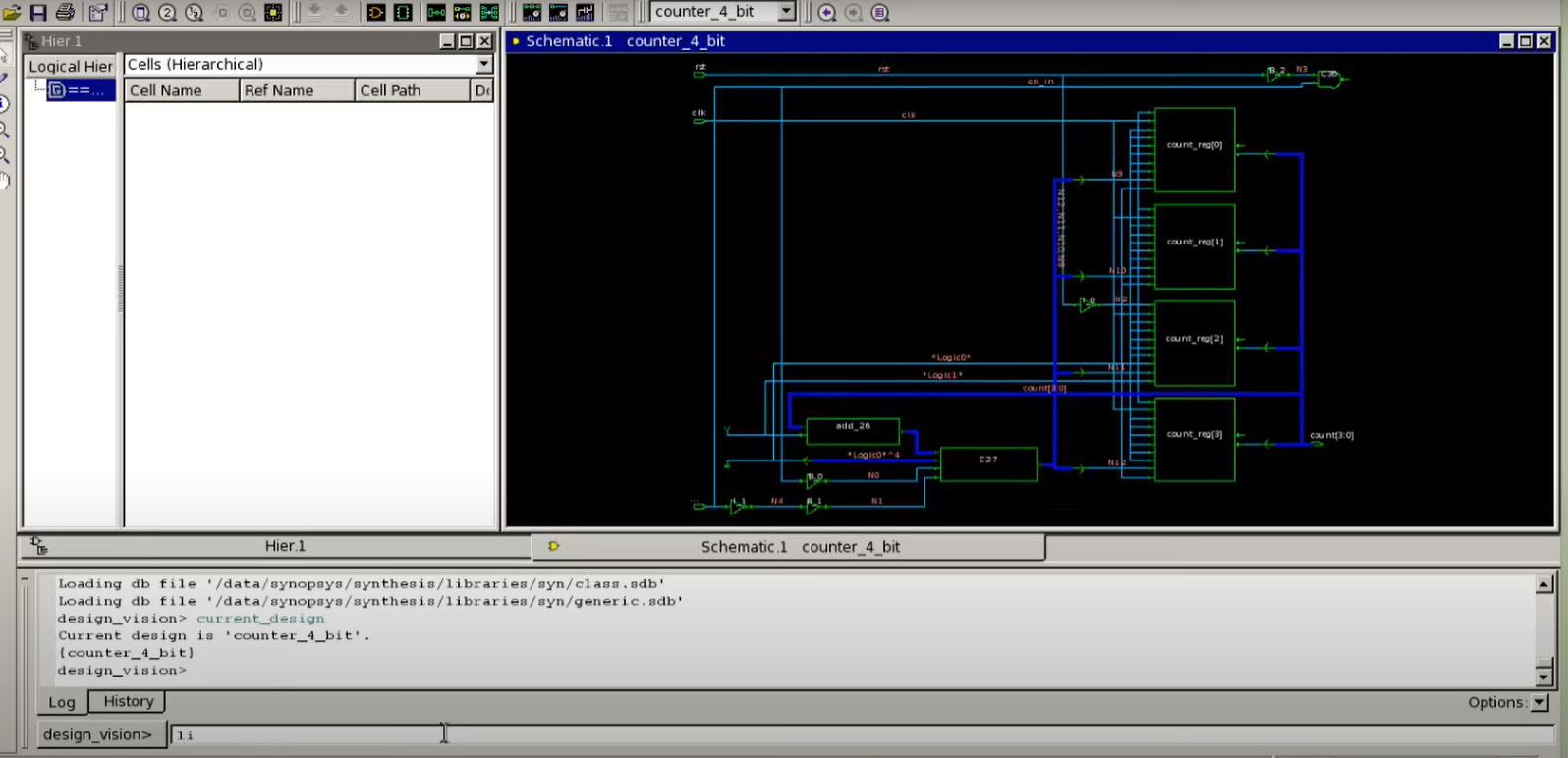

An example of a Synopsys tool used to compile a chip design:

During the chip design process, regular rounds of running simulations take place to find bugs and other errors. When a design is nearing completion, the chip can also be emulated on physical hardware so that accompanying software can already be tested on top of it. This way, you can further develop your hard- and software in parallel alongside each other.

So we have two phases in the testing of chip designs: simulation and emulation. Both Cadence and Synopsys provide emulation hardware, although historically, Cadence has been the stronger player here. Similarly, both players have been investing in simulation software, with historically Cadence being stronger in analog and Synopsys being stronger in digital ICs. However, over the years they’ve been moving into each other fields.

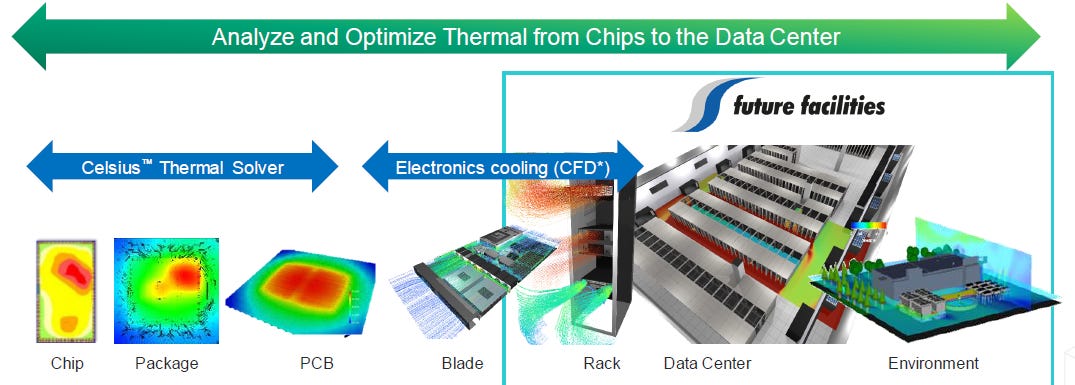

Examples of some of the simulations you can run on Cadence’ tools are shown below. You could thermally simulate for example how much heat the different parts of a chip are generating, and do the same for the entire package, the PCB, the server rack, and the entire datacenter:

Cadence has also been moving into simulation of wider systems. For example, analysis on computational fluid dynamics (CFD) was provided for the McLaren Formula 1 racing car. So the company is really competing here with Ansys’ historical core business. And recently via acquisition, the company has also moved into molecular simulation used in the drug discovery market.

Overall, Cadence has been building up an impressive simulation portfolio, which could play a role in the decision of Synopsys to take over Ansys. Historically, Synopsys has been investing more in its IP portfolio, i.e. the Lego-like building blocks of semi design, and the company has built up successfully a large portfolio here.

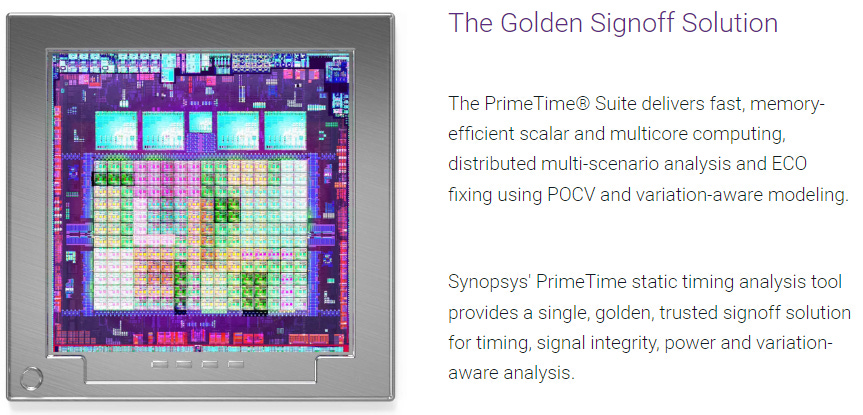

In simulation, Synopsys has the PrimeTime suite, which can provide simulations of path timing, signal integrity (identifying issues such as voltage drop, noise, and crosstalk), and power consumption per chip area.

Clearly there is quite some overlap here with Ansys’ tools, and so if the regulator determines that the new entity’s combined market share will be too dominant, this could be an obvious motivation to block the deal. Especially as the FTC under Lina Khan has become hawkish, especially when it comes to approving tech deals.

Under previous administrations, the FTC had been quite dovish, frequently allowing large-scale M&A within the same industry. For example, they gave the Linde-Praxair merger the green light in 2018, although both these companies have fairly large market shares in the industrial gases industry. A deal would have much better chances of being approved should the Trump administration return to the White House next year, so even if Lina Khan blocks the deal this year, there is the option for both companies to retry next year under that scenario.

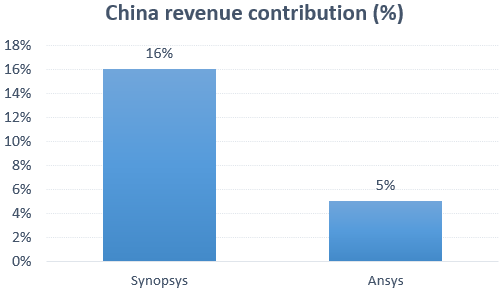

The other potential stumbling block for this deal is China, which recently blocked the takeover of Tower Semi by Intel, likely in retaliation for the high-tech export restrictions the US has introduced on China. The CCP currently has limited options to fight back, so blocking US mergers and acquisitions is one way they can put some pressure on the US business world.

A lever that Synopsys and Ansys can use here, is convincing the Chinese that a combination of the firms can accelerate semiconductor design in China, which is obviously a key priority for the CCP. The company could also make other promises, such as investing in training centers for semiconductor design at Chinese universities.

China is significant for both players in terms of revenues, so getting the approval will be necessary. When China tried to block the ASML acquisition of Carl Zeiss’ optics division a few years ago, ASML simply told them that they would stop selling China lithography tools and would go ahead with the deal anyways, after which approval was quickly granted. So this could also be an option for Synopsys and Ansys, given that they have a number of dominant tools in IC design and simulation..

So there are a number of potential roadblocks to this deal getting over the line, something which is useful to keep in mind especially if you’re long Ansys. Synopsys on the other hand is down 12% since announcing the deal, so you should actually get upside if the takeover has to be halted.

Synopsys’ CEO commenting on the likelihood of this deal getting regulatory approval:

“We did not jump into this combination without a clear expectation that the regulatory review will be manageable, we were fairly well advised and we both are very committed to closing this deal. Now regarding specifically to China, I really don’t want to speculate at this point regarding the process. As you know, the vast majority of Ansys’ products are not subject to the US export licensing requirements.”

The Ansys - Synopsys deal

Both companies have actually already been working together since 2017, with Synopsys’ Fusion Compiler and 3D-IC Compiler integrating Ansys’ RedHawk. Today, the vast majority of Synopsys’ installed base on these products already incorporates Ansys’ simulation platform. So although Synopsys has simuation capabilities as well as highlighted above, it is clear that Ansys has a much wider offering as the strongest player in this space.

Ansys has been integrating with other vendors as well, for example at PTC’s capital markets day, Ansys was almost as much on stage as PTC’s management. Ansys’ philosophy has been to work around open interfaces, so that best-of-breed software solutions can easily work together, exchanging data-based models between them.

Synopsys’ CEO going through the rationale of this deal:

“The complexity of system design is driving our customers’ needs for the fusion of electronics and physics augmented with AI. We’re combining a leader in semiconductor design technology with a leader in simulation to address this rapidly emerging customer need.

This transaction will enhance our silicon to system strategy, both across our core EDA segment and in highly attractive adjacent growth areas where Ansys has an established presence. Megatrends are pushing the need for advanced chips and new system design methodologies across verticals such as aerospace, automotive and industrial equipment. The world of semiconductor design and physical simulation must come together to ensure interconnected systems function properly in real-world settings.

Semiconductor companies must now design in a world of high-performance computing with a system approach in mind. Similarly, systems companies must move down to the silicon level to unlock value with purpose-built chips and software-defined systems. This is creating new complexity challenges that this combination will help solve.

You’ve been hearing us talk about the electronics digital twin. In other words, how do we create a model for these chips so system companies can run their simulation early and develop their software early.

Our customers are moving from monolithic chips to multi-die systems. These systems are so dense and so complex that they require not only power integrity but sophisticated structural, thermal, and electromagnetic analysis to deliver high-performing chips. Joining forces with Ansys is the next logical step.

On day one, we will significantly extend our portfolio of solutions that we can offer as we work on our integrated products roadmap. We expect the combined company will benefit not only from immediately accelerating the penetration of high-tech customers through cross-selling opportunities, but also in other high-growth adjacent verticals that are demanding multi-domain solutions such as in aerospace, automotive and industrials. Ansys has significant presence in these underpenetrated verticals and represents a huge opportunity for the combined company.

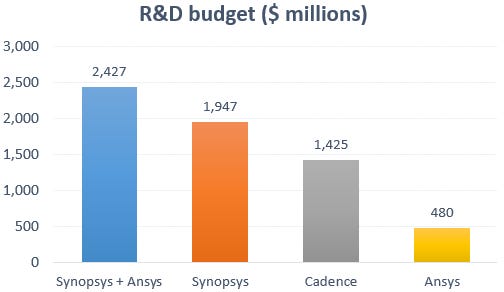

This combination is expected to increase our TAM by 1.5x to approximately $28 billion. We expect this combined TAM to grow at 11% annually through 2028. Given the capabilities of the combined company, we expect to grow revenue faster than the TAM. We will have an R&D budget that’s approximately 2x the median of industry peers.”

On the final point, the combined entity would certainly become a dominant player in the industry in terms of R&D budget:

Promised synergies in mergers frequently have disappointed. However, as more systems companies are moving into designing their own custom silicon, there could be leverage here for Synopsys to grow their business as these companies tend to be big Ansys users already.

On the other hand, typically semi designers will leverage tools from all three of Cadence, Synopsys and Siemens, taking the best point solution for each task and pipelining them together. This could be about to change however, as we noted previously that with an increasing number of workflows being driven by AI, the AI engines frequently make use of the broader suite of software tools from a given EDA provider.

So going forward, it is possible that customers will more frequently opt for what they see as the best suite, as opposed to pipelining best of breeds. In such a scenario, the Synopsys - Ansys combination can have an advantage here due to Ansys’ strong positioning in simulation.

Financial model of the combination

Synopsys’ CEO went over the terms of the deal on the call:

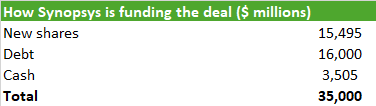

“Synopsys will acquire Ansys for $197 in cash and 0.345 shares of Synopsys common stock per share of Ansys. Following close of this transaction, Ansys shareholders will own approximately 16.5% of the combined business. We intend to fund the $19 billion of cash consideration through a combination of cash and debt and have obtained $16 billion of fully committed financing. We are targeting to close in the first half of 2025 subject to customary closing conditions, including receipt of regulatory approvals.”

At this moment the risk is balanced for Ansys shareholders, 12% upside over the coming year if the deal closes — assuming Synopsys’ share price stays where it currently is — and 11% downside should the deal get blocked. However, given that the Ansys board has put the company up for sale, there is still scope under the latter scenario for a private equity buyer to come in, limiting the downside. And if the business doesn’t get sold, I believe Ansys will continue to be a good investment anyways over the long term. Should there be a sell-off in Ansys shares if the deal falls through, they will likely be interesting to pick up for long term investors in my opinion.

Synopsys’ CFO detailing the expected financials post transaction:

“The transaction is expected to immediately expand margins, increasing Synopsys non-GAAP operating margin by approximately 125 basis points for the first year post close and by approximately 250 basis points in the medium term. In addition, we expect to realize significant synergies: $400 million of identified and actionable run rate cost synergies by year 3, $400 million of run rate revenue synergies by year 4, growing to over $1 billion annually in the long term. We believe the transaction will be accretive to non-GAAP EPS within the second full year post close and financially accretive thereafter.

At transaction close, we expect our gross debt to adjusted EBITDA to be approximately 3.9x. Subsequently, we expect to generate substantial and sustained free cash flow, which will enable us to rapidly delever to less than 2x within 2 years of the transaction close. Our long-term gross leverage target is below 1x, and we expect to maintain investment-grade credit ratings, given our strong cash flow generation and commitment to rapidly delever. We intend to resume buybacks as we approach our leverage target of below 2x.

On to our combined company long-term financial objectives. Our goal is to drive shareholder value by delivering annual industry-leading double-digit revenue growth, non-GAAP operating margins in the mid-40s, unlevered free cash flow margins in the mid-30s, and high teens non-GAAP EPS growth.”

A full model on the combination is highlighted below, working all way through how this will impact EPS for Synopsys shareholders. I reach an IRR of 22% working from Wall Street consensus estimates, which I think should be do-able and beatable, and then modelling in some guided synergies.

Currently, the shares are trading on 29x adjusted 2025 EPS on these estimates, whereas Synopsys has typically been trading around 38x forward EPS over the last years (chart below).

As the company is raising debt for the acquisition, it can’t offset dilution from SBC with share buybacks in the coming years, so I modelled in annual dilution as from ‘25. You can also see the impact on the share count from Ansys shareholders receiving shares.

Synopsys’ forward PE over the last years, bottoming at 30x in late ‘22 and with a median of around 38x:

Synopsys is financing this deal with a bit more than $15 billion coming from the issuance of new shares, $16 billion from raising debt, and $3.5 billion in cash:

Overall, looking at the risk-reward in both shares, on my analysis Synopsys should be the most attractive one to hold of the two, as there shouldn’t be downside if the deal falls apart while investors should be able to make a handsome return over the coming years if the deal goes through. Additionally, the shares should be a good investment if Synopsys has to continue solo.

If you enjoy research like this, hit the like button and subscribe. Also, please share a link to this post on social media or with colleagues with a positive comment, it will help the publication to grow. All shares are appreciated.

I’m also regularly discussing tech and investments on my Twitter.

Disclaimer - This article is not a recommendation to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it can not be guaranteed that all information used is of this nature. The views expressed in this article may change over time without giving notice. The future performance of the mentioned securities remains uncertain, with both upside as well as downside scenarios possible.

Loved reading this!

Tech Fund that was detailed and great analysis!