Industrial analog semis, Texas Instruments vs Analog Devices

Industrial analog semis, Texas Instruments vs Analog Devices

An overview of the space

The attractions of the industrial analog market

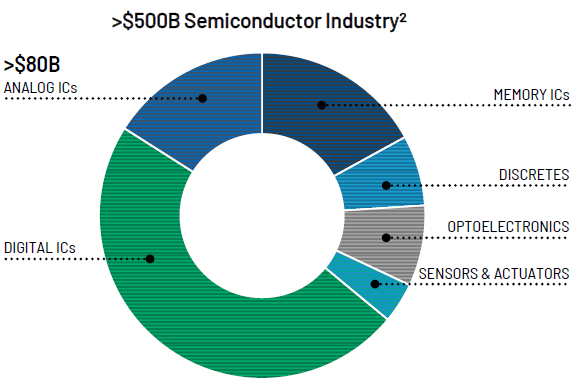

In the $500 billion-plus semiconductor market, analog sits as an attractive niche. New entrants are not common in the space, margins and revenue growth can be attractive for the best quality companies, and product lifetimes can last for even multiple decades, giving resiliency and attractive cash-flows in the cyclical semiconductor industry.

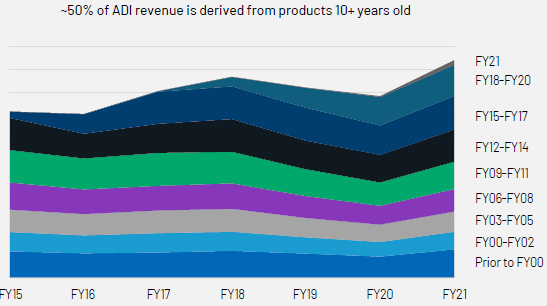

Within analog, the industrial end-market can be particularly attractive due to extremely long product lifetimes. For example, for Analog Devices (ADI) — a player focused on this end-market — 50% of revenues stem from products over 10 years old:

This means that sunk capex can generate cash-flows for extremely long periods of time, as semicap equipment doesn’t tend to break down. ASML for example estimates that practically every tool they ever sold is still in use.

These long product lifetimes make it also especially hard for new entrants to break in into these markets, as you can only very gradually build up revenues at the rate of sockets opening up for new products.

Additionally, there is much less focus on analog semis in academia, so you have to learn how to bake these semis on the job, which I’m being told is somewhat of an art. This again makes it harder for new competitors to start competing, as opposed to for example in digital semi design, where it is much more straightforward to start a business due to the comparatively higher availability of engineers combined with a capital light business model.

As investors, we also get no customer concentration risk as we have with TSMC for example where Apple, Nvidia and Qualcomm are very significant customers. On the contrary, the large players in this field typically sell around 100k different SKUs to a similar amount of customers.

Pricing power is actually decent for the quality companies in these fields, as due to the long product lifes, some price increases can be implemented over time. The typical analog semiconductor sells for less than $0.5 per piece, so cost reductions are not an area of focus for customers here, especially for manufacturers of highly-priced industrial equipment or automobiles. The other source of price increases is innovation, as more advanced products sell at higher ASPs when they are introduced.

ADI’s CEO, Vincent Roche, discussed their pricing strategy at the UBS conference:

“So typically, when we get a design established, in the industrial business, those sockets will last for 17 years on average. And then consumer is somewhere between 3 and 5 years. But when we get the socket, the pricing is very steady over the life of the product. So these are very sticky products and there’s many places in which we play, so there’s a tremendous diversification.

But the price increases that we put on our customers during ‘21 and ‘22, they will stick largely. If there are price decreases in the portfolio over time, that has been agreed upfront and that tends to be based upon a volume to price relationship. So if the volume occurs that we’ve agreed upfront, there’s a certain price reduction associated with that. But there are parts of the portfolio as well, where we actually increase prices over time, typically older vintages that we maintain for 20 to 40 years.

Over the last couple of years, we got half of our growth from pricing, basically repricing our products to the level of inflation that incurred in our cost of goods. But generally speaking, we’re adding more ASP value to our portfolio every year. We’re doing that through innovation. For example, our 5G transceiver technologies compared to 4G. We also are able to add some software value to the products, that gives us a little more ASP again.

So new products in particular, we’re increasing the ASPs. 7 or 8 years ago, every year we would face probably a 5% price concession compared to the prior year’s revenue, those days are finished. So that’s very stable now.”

The other big player in this field is Texas Instruments (TI). TI’s new CEO, Haviv Ilan, a 24-year veteran at the company, discussing their views on pricing and where to play in the market at the Bernstein conference:

“We’ve learned that the higher the ASP, and the higher the volume per socket times ASP, the more competitive the market is. It’s hard to maintain margins. When you serve a $0.25 to $0.30 a socket, price is not the biggest thing. It’s performance, power and feature of the part. We make good margin on this.”

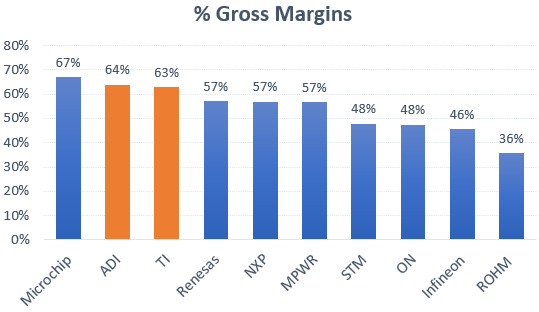

The quality of a semiconductor manufacturer is often measured by the strength of the gross margins, the difference between what you sell the semiconductor for and how much it cost to manufacture it. Both ADI and TI are among the best in class on this measure, which has been translating into attractive FCF generation as we’ll see later.

These high margins are no surprise as both ADI and TI have been orienting their business towards the more attractive parts of the market, both via M&A as well as internal R&D.

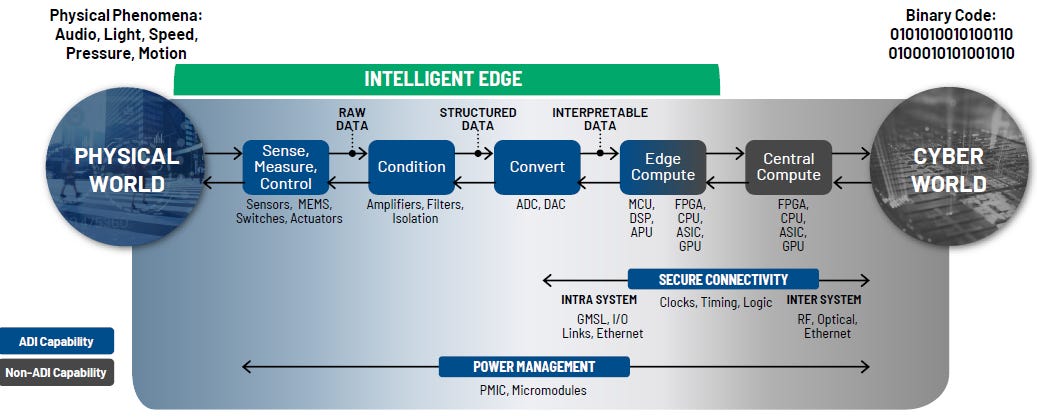

Analog semis are used to measure the physical world, such as temperature, pressure, and audio. So unlike digital chips, where transistors can take on two states i.e. 1 and 0, analog transistors take on a continuous range of values to reflect these real world measurements.

An analog semiconductor consists of multiple transistors, connected to achieve the desired functionality. A variety of analog semis are connected in a typical system, converting these measurements to provide signals to a digital computing unit, which uses this information to perform calculations and send instructions to the output systems.

Analog semiconductors can perform a wide variety of tasks, such as amplification, filtering, and signal conversion. And they are also used to manage power in electronic equipment, i.e. PMICs or power management integrated circuits.

ADI illustrates the variety of tasks their products can perform in a typical workflow:

An image of a MaxLinear PMIC on a Raspberry Pi:

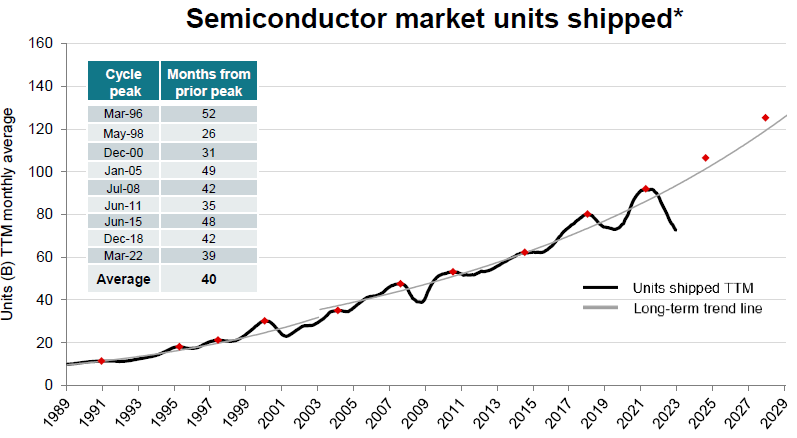

Looking at end-market demand, both the number of products making use of semiconductors has grown, as well as the semiconductor content per product. Semiconductors are taking on ever more tasks, from heating the seat in your car, to the same seat massaging your back, to providing you with an operating system to control your car and play a video game.

As such, the number of semiconductors being shipped annually has been on an attractive, upward-sloping trendline (chart below). And although the semiconductor industry has been going through one of the most severe downturns in its history over the last few years, TSMC’s and ASML’s commentary last month indicated that we are on the cusp of new bull cycle.

To illustrate this, ADI shows how its semiconductor content in robotic arms is increasing:

Most semiconductor firms have been providing similar charts for automobiles, and it won’t stop there. ADI illustrates how every decade, the demand for computing power has been increasing:

And according to the data from ADI, analog has even outperformed digital in terms of revenue growth:

So despite the low ASPs and somewhat ancient technology for semiconductors — as analog semis are manufactured on process nodes of around 90 to 300nm — analog firms can actually hold several attractions. Especially for investors looking for cash-generative and compounder-type stocks, as both ADI and TI are committed to return all free cash flow to shareholders, in the form of both dividends and stock buybacks.

Texas Instruments (TI)

TI remains the top player in mature semiconductors, so this is a good place to start. Note that all companies in the chart below aren’t necessarily directly in competition with one another. There will be some overlap, but they will also be focused on their particular verticals. For example, Infineon and STM have large discrete businesses — power semiconductors, i.e. switches, not to be confused with PMICs — where TI and ADI don’t compete, or at least don’t have a large business based on the market share I’ve seen. A lot of these players will also have microcontrollers however and there will be overlap here.

74% of TI’s business is now focused on the industrial and automotive end-markets:

TI’s CEO discussing the industrial business at the Bernstein conference in May of last year:

“Factory automation, the return on this is immediate, like in one year to 18 months, you already return the investment of the robotic arm or the AGV, and just save on labor. So that is something that is accelerating. Labor is hard to get, there is also inflation, so you replace it with machines. So that’s an area where we see great opportunity.

Electrification is a big part of industrial, it’s now probably our fastest-growing sector. If you just look at solar energy, from the panels to the inverters, to the storage system and distribution, these are thousands of dollars of opportunity per system for the company. And it’s very early in the adoption curve, growing very fast.

So these are a couple of sectors that are examples of our industrial business, but there are hundreds of them. And every one of them is being redesigned into more electric, a more electromechanical system, whether it is mechanical or gas based, so we are excited about that.”

So he’s only scratching the surface here as TI’s semis go into 13 industrial sectors, from electric grids to trains, aerospace & defense, medical, motor drives etc. The other big part of TI’s business is automotive, the CEO discussing this opportunity:

“Automotive has actually been the fastest-growing business for us in the last 10 years. It’s an end market that we define with five different sectors, those include ADAS, powertrain, infotainment, body electronics, and lighting. And a typical ICE vehicle has around $400 of content. If you go to an EV, that doubles or triples in some cases, hundreds of sockets. This is why you won’t hear us talking about one end-equipment, whether it’s battery, DC to DC, onboard chargers or traction inverters, we play in all of them in a material way.

When you look at the board in the automotive market, you see the breadth of the parts. We are also internally teaching the team to stop talking about specific sockets because the broad opportunity, they add up. You don’t want to just put all the efforts on the one, two big sockets, rather the entire board. Think about the lights, ambient lighting, the seats, and the massages — 18 motors in a seat, it’s the record I’ve seen. And each motor has to be driven, has to be sensed, has to be controlled, has to be powered. The breadth of the opportunity in a vehicle is immense.”

TI really expanded in automotive thanks to the National Semiconductor acquisition in 2011. This also highlights that organic entry is not simple, and typically analog companies have gone into new fields via M&A as you quickly get scale and a wide product portfolio to compete in the market.

The other part of TI’s business are embedded semis, which are microcontrollers, connectivity semis, and radar sensors:

TI’s manufacturing strategy is to leverage its scale to give the company a permanent cost advantage with its 300mm strategy. The larger the wafer, the lower the cost per chip as larger wafers allow for more dies to be processed at once.

A lot of manufacturing in the mature semi space still happens on 200mm, and even 150mm, so TI decided to move to 300mm wafers thanks to their large scale, just like the advanced manufacturers in leading edge semis are doing i.e. TSMC, Samsung and Intel.

To illustrate this strategy, a one dollar chip can be manufactured for $0.20 on a 200mm wafer, but for $0.12 on a 300mm one, giving TI a 40% cost advantage compared to most competitors. Although when you include the cost of packaging, the advantage is reduced to 20%:

Only the really large scale players can implement this strategy as you need a lot of volumes to transition to 300mm. Infineon has been implementing the same strategy in its power semiconductor business, and this company is obviously one of the titans as well in mature semis.

TI had 40% of its manufacturing on 300mm last year and is expecting this to move to above 80% by 2030. Similarly, the company is moving all its production in-house, last year only 20% was manufactured by outside foundries and this will be reduced to 10% over time. This is actually the largest difference in strategy with ADI as we’ll see later, who has its manufacturing more evenly split between its own fabs and external foundries.

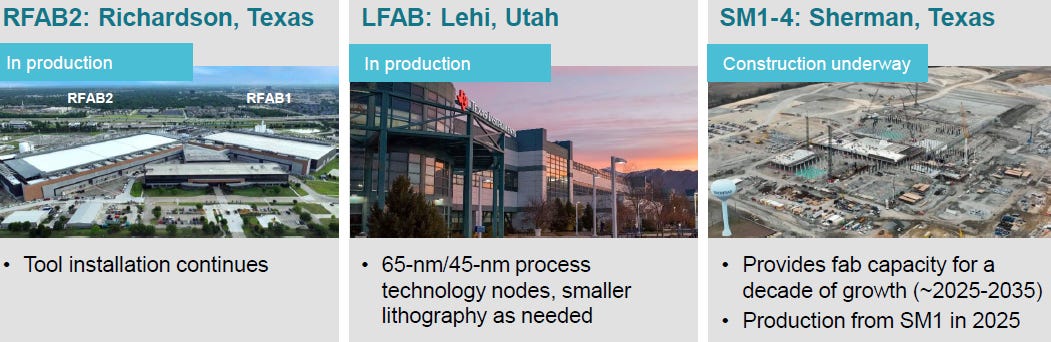

Due to this manufacturing strategy and TI’s growth bullishness from their conversations with clients, TI has become a current capex and future free cash flows story. This introduces some risk, although due to the extremely long product lifetimes and high growth in the semiconductor space, the risk seems low that this capex will be wasted. Worst case scenario, the newly constructed fabs in Lehi and Sherman get filled more slowly than anticipated. And as you can also gradually bring in the equipment as the design wins come in, the risk that these fabs will be poor investments is reasonably low in my view.

The Lehi fab’s purpose is to bring the embedded business in-house, i.e. microcontrollers and other digital semis, so therefore this is 45nm to 65nm capacity. This fab and the equipment was purchased from Micron on the cheap when it exited the 3D-crosspoint business.

TI’s CEO discussed at the Bernstein conference that the ramp here has been ahead of schedule due to strong demand still for embedded products. And he also discussed the Sherman fabs at the same conference, this is a site where four! fab shells can be constructed:

“We are going to build the first two shells in parallel. We want to be ready with the brick-and-mortar ahead of the equipment. Our RFAB2 will ramp to full production somewhere in 2025, and we will want to have Sherman 1 continuing that growth in the middle of ‘25. And Sherman 2, it depends.

And TI, by the way, we don’t like to spend money. So when we do it, we look very carefully on what’s the risk versus reward. Somewhere in ‘25-‘26, when I would say where see through the next cycle, we can have a checkpoint and say ‘hey, are we ahead of ourselves, should we slow down the investment plan?’, and we have the option of how we want to invest.

We prefer to be two years ahead with supply rather than two quarters later because it’s very painful and we felt it during the covid cycle, when you don’t have enough supply to support your customers.

Even in 2019, when we decided to continue with RFAB2, the same people said ‘are you guys crazy?’ Oh boy, if we had that factory ready a couple of years earlier, that would have been a great moment for TI. But I think the opportunity will come in the future.”

So it’s clear that not being able to fulfill the demand during covid has been an input factor in the decision to step on the gas in terms of capex investment. TI is planning to spend $5 billion on capex per annum over the ‘23-’26 years with investments of around 10 to 15% of revenues thereafter. Although the company is also expecting some of these investments to be recouped quite quickly in the form of subsidies from the CHIPS act. Benefits will be accounted through the P&L in the form of lower depreciation, raising earnings, while the cash will be added on the balance sheet. These are very meaningful benefits, as the company is expecting $4 billion of this $20 billion investment to be recouped.

With this overall capex plan, the company will be able to support $45 billion of revenues by 2030, generated from over 90% internal manufacturing and over 80% on 300mm:

In the financials section, we’ll model out what these capex plans mean for free cash flow generation. In the meanwhile, here’s TI’s CEO discussing at Bernstein why’re they’re so bullish on growth, and are guiding for TI to grow at a 10% CAGR over the long-term:

“Just look at what industrial and automotive did for us, if you go back to 2013, it was 42% of our revenue and it was 65% in 2022. You can do the math, industrial and automotive grew at almost 11% [per year], and that’s where embedded did not have its best days. So before we put all the R&D effort, acceleration into these markets, before we got to learn these markets in granularity, we have overperformed.

We are seeing an acceleration of secular growth in industrial and automotive, and it’s accelerating with EVs and you see acceleration in industrial in areas like factory automation, medical, aerospace and defense, and electrification. If you just take the same growth rate from 2022 for industrial and automotive, and just hold all the other markets flat, you'll get to about 8% growth for TI. So 10% doesn’t sound crazy when you do that math. Of course, it looks weird because we’ve not done it before, but this is where you have to look under the hood and see where the opportunity is.

And then the feedback of the customers, which is a big part for us because when we came out there with a 7% growth plan and showed the investments, the feedback of our customers was ‘we think we need more’. And when talking with customers about ‘25 and ‘30 and what they are willing to do with TI, this gave us the confidence that we want to take that plan to 10%. We want to support $45 billion of revenue by the end of the decade and to do that, we have to start to invest now.”

While the semi manufacturing fabs are being built in the US, packaging operations are spread more around the globe, such as in Malaysia, the Philippines and Mexico, bringing the final product closer to the manufacturing customer.

Typically, mature-tech semi manufacturers have a substantial proportion of revenues coming from distributors, who sell the packaged semis to the end customers. These types of semis are also called catalog items as they can go into a variety of products. So you can buy amplifiers, filters, converters, etc off-the-shelf. Distributors can easily make up 50% or more of revenues for some semi manufacturers. For example, for ADI, 61% of revenues last year was sold through the distribution channel.

Also here, TI has been taking this part of the supply chain in-house with its ti.com website, the Amazon of analog semis if you will. This e-commerce website is linked to automated warehouses from where orders can be shipped. We’ve discussed previously how TI automated its Singapore warehouse with the Autostore robotic system:

“After Texas Instruments installed the system in one of their warehouses in Singapore, they were able to consolidate three warehouses into one as the inventory capacity of the warehouse went up fourfold.”

TI’s CEO discussing the rationale for ti.com:

“We’ve made the change long ago to own and control our sales and marketing portion of finding chips on board, and when we did that, we found a lot more sockets around boards that were apparently there. Now you’ve seen this investment that we’ve been making over these years to improve, making it really easy to do business with TI. The ability now to do large order quantities, being able to do things like local currency transaction, importer of record, that messy stuff that you wouldn’t want to normally do. And what it means for a customer, if you want to have a part tomorrow, you can do that. If you want to order directly through TI, you can do that. And if you like to still order through a distribution partner, you can do that too.”

As a result, TI’s direct revenues have gone up from 35% in 2019 to 75% in 2023:

Also the R&D strategy is worth discussing, as this is one of the levers for growth. The company’s CFO at UBS:

“Let me give you some angles to R&D. One is geographically, we have the largest R&D centers in Dallas, we have large centers in Santa Clara, from the National acquisition, and we also have a really large center in India. They do great work and we’re expanding there.

Another angle is how that R&D is deployed, the bulk of it is from the product lines, so they work with sales and marketing, with customers, and they release families of products. We release 400 to 600 products per year.

Another bucket is process technology, and they’re releasing the recipes for the next level of processes, the product lines we’ll eventually design on. And we have 10 different families or more of process technologies. And then every year, we upgrade those a little bit by changing different features that the designers can use.

Alongside process is packaging technology. So because as you make the chips smaller and more efficient, the package becomes a really important feature as it needs to be able to dissipate heat.

The other angle is Kilby Labs, after Jack Kilby, the Nobel Prize winner who was an employee at TI many years ago. Those are about 80 PhDs who work on things that are not directly tied to revenue. So they’re not releasing products, but they’re working on concepts that when one of those things works out well, eventually, we can take that to market through different products.”

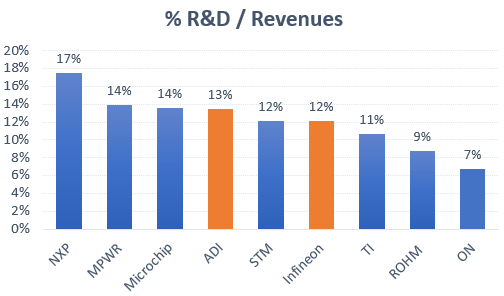

Mature-tech semi companies typically invest in the low teens of revenues into R&D and TI and ADI are no different:

Analog Devices (ADI)

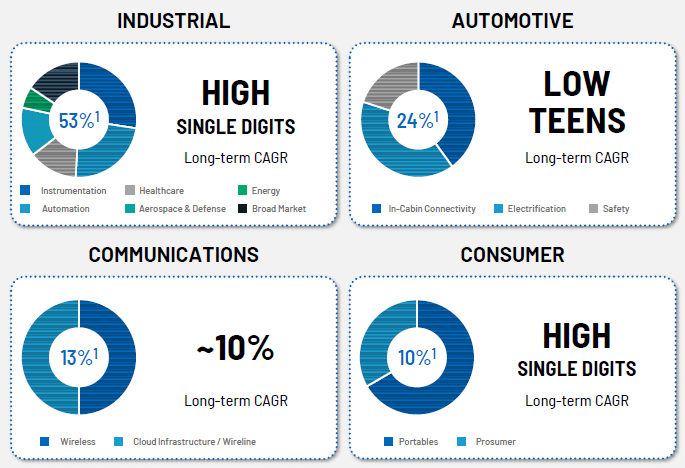

ADI has a very similar end-market split as TI, with 77% coming from industrials and automotive, and with smaller exposures to communications and consumer:

ADI’s CEO gave an overview of their business at the recent UBS conference:

“Automotive, it’s been a business that has been using more and more of the electronics for in-cabin experience, electrification of the vehicles, with battery management systems, safety systems, and power management. So it’s quite a diversified business for ADI. When I look into ‘24, I still think automotive will be the strongest segment for ADI. We’re seeing 10% to 15% more silicon used in each new car platform and I believe that will be the case at least to the end of the decade.

And we’re benefiting from more sensors being used in cars, electrification, battery management systems. And we have two modalities there, both the more established wired technologies, and we’re now at the early inception of wireless technologies. And that creates a whole new growth trend for ADI. We have five major OEMs signed up for that technology, which is yet really to deploy.

Of course, the big governor is what happens to the SAAR (number of car sales). But we believe that if SAAR is flat for the foreseeable future, that we will still grow 10% a year. It’s content. And the EV sector is in the very early stages of adoption.

We see a big opportunity in factory automation, we have a big play there in terms of the connectivity solutions. We’re investing heavily in intelligence, robotics, and automation systems.

Aerospace and defense is probably the only area right now where we are seeing supply constraints, and we do a lot of high-speed technology development specifically for that sector. So that encompasses a lot of microwave technology and very high bandwidth data conversion systems.

In digital healthcare, we’re seeing an upsurge in the need for newer instrumentation, automatic test equipment, solutions for things like AGI and the new generations of datacenters that need to be built to handle AGI. Healthcare is now $1 billion within the ADI portfolio and we will split it out, it’s highly profitable and highly diversified. When we started really putting focus on this healthcare business, about a decade ago, it was sub $100 million. So this will be the 8th year of double-digit growth. So it's been very, very strong. Everything from clinical grade vital signs monitoring in the hospital, now moving into the home, and x-ray and ultrasound systems. For example, in x-ray we are producing compound monolithic subsystems that reduce the size and take 5% of the energy to produce the equivalent image in the old systems.

Communications, the portfolio is roughly split half wireless and half wired today. Wired is really about cloud, the datacenter, optical communications. Our wireless business is communications infrastructure, 5G, and then there are many variants coming on 5G as well.

More and more of our products these days are using software and algorithmic technology. We have over 1,000 software engineers at ADI and we’re now bringing products to market that not only have algorithm routines, but we’re also putting machine learning, neural networking in more of our products. So if you take for example, power management, you’ve got very complex solutions and you’ve got to keep the power loops very stable and predictable. We’re using machine learning to provide more accuracy. So the hardware gets you so far, and the machine learning technologies help us tune with more accuracy. We use our digital business basically in everything that we do now, but stand-alone our digital business generates about $0.5 billion of revenue. But we figure it’s more meaningful to report now by end-market, so you don’t hear about the technologies as much anymore.”

ADI is seeing double-digit long term growth in automotive, high single-digit growth in industrial and consumer, and around 10% in communications:

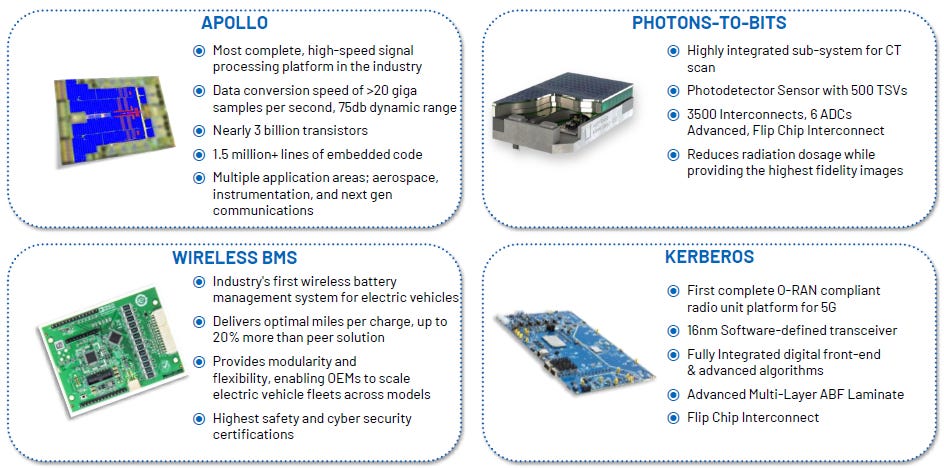

The below images illustrate how ADI is now also providing more complete systems, built around digital ICs and these pretty advanced actually, 3 billion transistors and 16nm technology are being mentioned for example:

These advanced digital semis are manufactured by outside foundries, so ADI does the design here. And also for analog manufacturing, the company is running a hybrid model. ADI has qualified external analog foundries so that they can easily expand volumes during cyclical upswings, while keeping their own fab utilization levels high during downturns.

This strategy was definitely an advantage during the covid semi boom, where TI wasn’t able to fulfill all demand, and ADI on the other hand could enjoy more brisk growth. The strategy also limits risk, as this more capital light model requires less capex.

ADI’s CEO discussing their manufacturing strategy at Bernstein:

“So we run a hybrid model, we need process recipes for making our silicon that sit between 7 nanometers and 7 microns, that’s 1970s technology. We have products in the portfolio that are 45 years old believe it or not, and they are lithography insensitive.

We’ve raised our CapEx spend over the last couple of years to build more of the industrial products inside the company, so at 180 nanometers and above. We spent about $1.5 billion by the end of ‘24 to have doubled the output in our fabs on the West Coast of the U.S. as well as Ireland. We are spending another $600 - $700 million to upgrade our capabilities in Asia, pretty much the test capabilities. We do very little assembly inside ADI.

85%-plus of ADI’s revenue today is on 180 nanometers and above, but we still use external sources. We were very fortunate to have good partners with us during the pandemic, to help us get the supply that we needed. And then, at 90 nanometers and below, all of that today is outsourced and it will be for the foreseeable future.

So what we’ve built inside ADI, our 200-millimeter wafers for 180 nanometers and above, everything else is outside. When demand is very strong and we run out of capacity internally, we raise the demand on our external partners. When the demand declines, we try to run our own factories to the fullest extent that we can. That’s how we get resiliency as well on the cost structure and the gross margins. With the new capacity that we have, we’ll be capable of probably doing 65% to 70% ourselves, versus 50% in the past. So we think in the aggregate, we can keep our operating profits at above 40% and keep our gross margins above 70%.”

ADI has done two large acquisitions over the last decade, acquiring Linear for $15 billion in 2016 and Maxim for $68 billion in 2020, consolidating the analog landscape. Linear especially was highly oriented towards maximizing gross margins, often missing new opportunities for growth. ADI’s CEO discussed how they’ve change this philosophy:

“We have instructed the business teams inside ADI, if we need to trade a point of gross margin to get a point of growth, go for the growth because that pays for many, many years to come. And to be clear, when the growth is there, there are opportunities to bring those margins up.”

ADI’s CEO also discussed the Maxim acquisition:

“We have the full breadth of technology that we need on the analog side. I’m thrilled with the acquisitions that we’ve done and what they’ve been able to bring to ADI. And we’re still in the relatively early stages of integrating Maxim, so that’s job number one. We’ve gotten the cost synergies, and we want to make sure we’ve got the revenue synergies, we said $1 billion by 2027.”

An overview of some ADI’s large customers, obviously a lot of interesting names:

The analog cycle

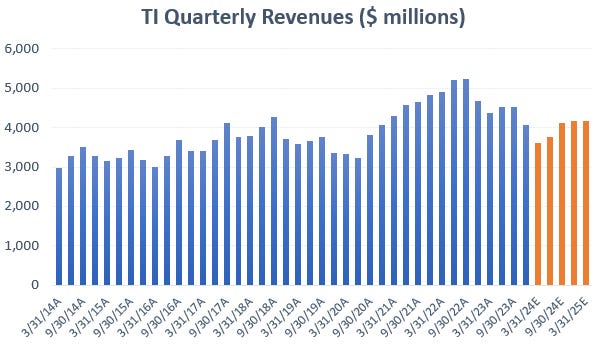

After the covid semi boom, the current downturn in analog has been particularly brutal, as next quarter will be the sixth quarter of revenues being on a declining trend for TI. On the positive, TSMC came out with a really bullish outlook for semis for ‘24, and although this is more driven by AI and datacenters, the industrial end-market could start benefiting as well. Wall Street is expecting revenues to bottom during the next quarter, after which we should see a gradual recovery:

ADI’s CEO discussing the state of the cycle at the recent UBS conference:

“Our bookings got back to a more normal pattern, lead times are back to normal with more than 95% of our products now shipping with 13-week lead times. So that gives customers the opportunity to decrease the amount of inventory they hold on their balance sheets. They see normality being restored.

In terms of what performed more weakly than we had expected, is really the industrial sector. And it was really the factory automation part that performed at a rate that was a bit of a surprise to us. But within that, it was the small- and medium-sized enterprises that suffered most and I think a lot of that is attributable to the rising interest rates, our customers are protecting working capital essentially.

We know that we’re undershipping our largest customers. The analysis shows us that we’re shipping at a rate that’s below their sell-through. And we run ADI on a POS signal. So we pay very close attention to what’s happening in terms of sell-through. We don’t look at sell-in, that’s a second order derivative. We set up our factory outputs based on what we believe the POS signal is telling us, and we’re also keeping the channel lean while keeping more inventory on our balance sheet.

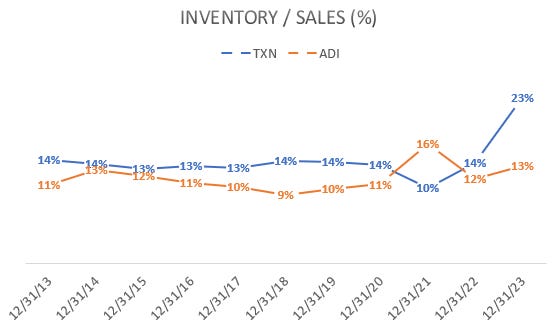

ADI’s current increases in inventory are still fairly normal when comparing them to sales. TI especially is very bullish on growth and therefore has been building up a big chest of inventories to sell into their end-markets when the next upswing starts. Currently TI has $4 billion in inventories on the balance sheet and they mentioned taking this another $500 million higher.

Inventories in the channel, i.e. distribution and end-customers, should clearly be on the decline, and normalizing, as ADI’s CEO mentioned they’re currently undershipping in the region of 15 to 20%.

TI’s IR discussed the cycle on the earnings call in late January:

“Our results reflect increasing weakness in industrial and a sequential decline in automotive as customers work to reduce their inventory levels. Similar to last quarter, I’ll focus on sequential performance as it’s more informative at this time.

First, the industrial market was down mid-teens as we saw increasing weakness. The automotive market was down mid-single digits after 3.5 years of very strong growth. Personal electronics was about flat and communications was down low single digits. Lastly, enterprise systems grew low single digits (these are datacenters).

And as the guide would suggest, we believe that we’ll continue to operate in a weak environment and one where customers are continuing to rebalance their inventories overall.”

So this outlook sounds like bottoming next quarter might be a bit optimistic, however, I do think we should see a bottom in a number of quarters, barring a wide global recession.

On the inventory build-up, as these are catalog parts which don’t become obsolete, their strategy should make sense. TI’s CFO explaining this:

“We’re very comfortable with our inventory level, we have a continued upward bias for at least one more quarter, probably a couple of quarters. But that is good inventory for catalog parts that sell to many customers and that last a long time. We are just in a different position than we were even 3 or 4 years ago in terms of how much of our revenue and our parts are in industrial and automotive, in catalog-type of parts. Our order fulfillment processes have also improved, we have ti.com that we can leverage to go direct to market.

Our target inventory is set really by device. We look at things like how many customers are buying the product, what the buying patterns look like, and how long it takes us to manufacture the product. So it’s really a bottom-up plan, driving the target overall. And we want to have inventory positioned to support growth over the long term.”

The main risk? China is building up semi capacity

There have been some concerns that with China stepping up investments in mature semis, this would pose a considerable risk to both TI and ADI. A few things no note here:

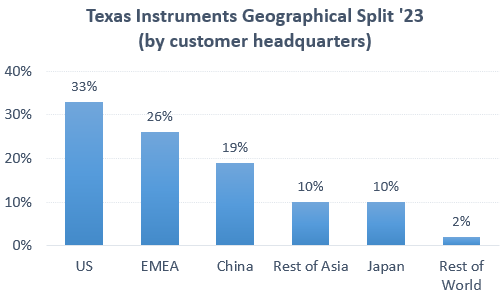

Firstly, although China is currently 40% of TI’s revenues, a lot of these are actually Western manufacturers based in China. So looking at revenue mix by customers’ headquarters, it’s actually only 19% of revenues which are currently coming from Chinese customers:

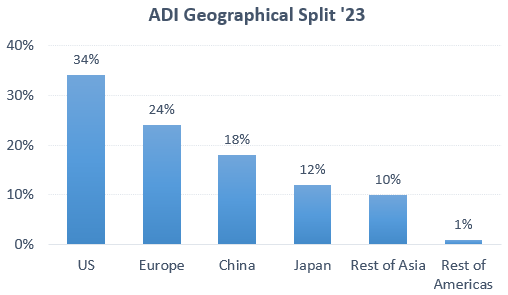

ADI reports a similar number of 18% revenue exposure to China — I suspect they use a similar definition as the TI headquartered-based one, although the explanation in their annual report is a bit more vague:

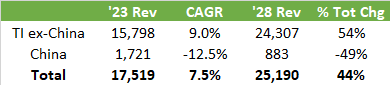

Longer term, with China investing in mature semis, it seems likely that market share losses with Chinese customers are likely. However, as the analog market continues to grow, these will partly be offset with growth of the overall pie. In negative scenarios, this is a part of the business that could indeed go down, however, even a dramatic scenario such as a 50% decline over the coming five years, would only result in a revenue headwind for the group overall of 1.5% per annum:

So if TI ex-China can grow at a 9% CAGR — which I think could well be possible — a dramatic 50% drop in the China-based business would still result in the group being able to grow at a 7.5% CAGR. However, I don’t think the declines in China will be that dramatic and with the growth in the Chinese analog market overall, this business could actually print decent results as I’ll explain below.

While it’s well possible that China has invested around $80 to 100 billion in fabs over the last few last few years, a whopping number, however note that this will be spread among a large variety of semiconductor types, from advanced logic semis of below 28nm, to mature logic capacity of 28nm and above, to DRAM, NAND, discretes, GaN, SiC, packaging, and analog. So let’s say around $8 to 10 billion went into analog, a not overly dramatic number.

However, even if I’m wrong on this calculation and the number ends up being higher, it’s not easy to gain market share in analog as discussed above. Product lifetimes in industrial and automotive are fairly long, so not that much sockets open up in any given year. Also, both TI and ADI compete at the high-end, having pruned their portfolios over the years, optimizing their exposure to the best quality and highest growth areas. Finally, both TI and ADI had to engage in large scale M&A to build up the product portfolios they desired, illustrating that it is not easy at all to gain organic market shares in analog.

Additionally, I think it is extremely unlikely that Western companies will source semiconductors from Chinese companies, making it hard for the Chinese players to break out of the local market, build up a large scale, and compete with TI and ADI in their bread-and-butter businesses.

A risk however could be that Chinese end-products, such as EVs and other industrial equipment, gain market share within their respective end-markets. This would allow Chinese semiconductor manufacturers to gradually gain share as well, being the suppliers to these market share winners.

I certainly think some of the Chinese EV manufacturers, such as BYD being one example, are fairly impressive. So I’m expecting them to take a certain share of the automotive market, just as the Japanese did during the ‘80s and the Koreans did during the ‘90s.

Anecdotally, I’m also regularly seeing reports that Chinese industrial equipment is becoming more competitive, which will certainly worry the Germans and other Western manufacturers. So these could form one avenue for the Chinese chip manufacturers to gain share.

ADI’s CEO discussing the competitive environment in China:

“Our business in China is distributed over several tens of thousands of customers and we deploy many tens of thousands of product SKUs. Once we get the design-ins established, those products tend to last. And ADI plays at the highest end of the performance spectrum, whether it’s industrial, automotive, healthcare, communications, as long as there is a market for high-performance technology, ADI will be the first choice.

We tore down a BYD EV, and people were surprised to see that BYD did their own battery management system. I believe there will be a continuing activity to displace foreign suppliers in China. But as we’re seeing today actually, if you look at our opportunity pipeline — which is the best leading indicator for what might happen in the future — that pipeline is increasing in size.

So we have sticky products, and yes, there will be places in the vertical market where the BYDs will be perhaps capable of building their own technologies, but again, I don’t expect that ADI will be displaced at the high end of that game. It takes a certain amount of scale to be able to verticalize your business, to build your own silicon, or at least design your own silicon and have it built. But the majority of our customers in areas like China are small and medium-sized and I believe that will be a merchant market for the long term.

There are really two markets in the analog space. There’s the commodity market, which is the lion’s share of the revenue pool, and then there’s the high-performance part, of which we have a very significant share as a company. You need to be precise, it’s very much a precision industry, high performance analog.

We have a very vibrant business in China and what I can tell you is that the engagements with our customers are still very, very robust. We’re still designing in across the spectrum of industrial and automotive applications. Communications, because of the geopolitical tensions, that changed the trajectory of that business (he’s referring to Huawei going south here following Western blacklisting).

Does it mean that certain parts of our portfolio could over time be converted? Sure. But 80% of ADI’s revenue is contributed by thousands of products that contribute less than 0.1% of the overall revenue. Where do you start if you’re going to compete with that portfolio?”

TI’s CFO similarly discussed the barriers that Chinese competition will have to overcome:

“First, we have our manufacturing technology, competitive advantage, and that’s the 300-millimeter best-in-class, cost-advantage factories. Then we have the broad portfolio, so tens of thousands of parts that go into tens of thousands of end applications. It’s very important to deal with a supplier that can provide you a broad set of parts, as opposed to twenty suppliers that each specializes in one vertical. And that’s what tends to happen with Chinese competitors, where they can get really good at one part. So in the industrial and automotive space, having that broad portfolio really plays well. Having that 300-millimeter cost advantage puts us in a position where we can compete in everything. Especially, in the markets we operate in, industrial and automotive, they don’t move share very quickly.”

So to conclude, I do think Chinese competitors will be able to build share and their portfolios over time, however, I also think the impact for both TI and ADI will be manageable as market share losses within the Chinese market will be gradual, and in a growing market. Whereas the business in the rest of the world should continue to be very solid.

Financials — TI share price $159 (TXN ticker), ADI $192

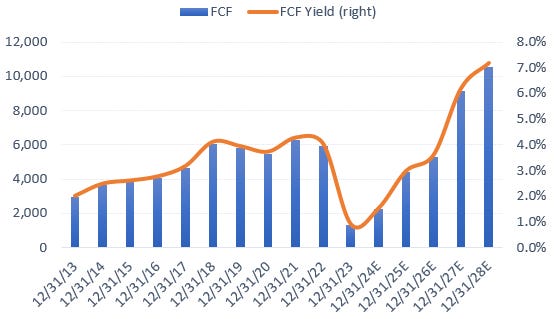

Let’s start with Texas Instruments. Currently TI’s capital intensity has been on the rise, they’re investing as they’re seeing strong long term demand from their end-customers. As such, the company’s long term guidance is for 10% per annum top line growth, an acceleration driven by the increased mix of industrials and automotive.

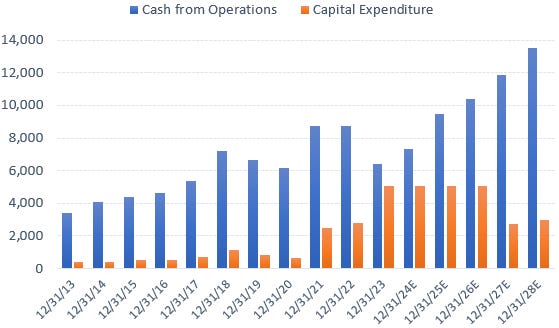

However, due the cyclical downturn in the semi industry, this currently is depressing FCF generation, which should now be getting close to a cyclical low. Overall, we could be looking at the following long-term cash generation profile for the company (chart below). For the ‘24-’26 period, I’ve taken the sell side’s estimates for operating cash-flow and then from ‘27 onwards, I’ve reduced the capital intensity in line with the guidance, with capex going to around 12.5% of revenues.

Note that the company is expecting $4 billion in benefits from the US government due to the CHIPS act, which I haven’t taken into account here. But I presume the government has given this figure as a guidance, as they mentioned this number on the recent call. This would mean that you could raise operating cash-flows for the coming six years years with around $650 million per annum.

If this scenario were to play out, TI will turn into a FCF machine in the long term, yielding 7%+ on the current enterprise value by 2028:

More near term and historically, the company’s financials and the sell side’s estimates are presented below. Looking at these, the shares are probably somewhat expensive in the near term, we’re looking at 21x ‘26 EPS and a 3% ‘26 FCF yield. However, the real appeal is once the capex starts rolling down as from ‘27-’28 onwards, hopefully, and this should bring the rewards.

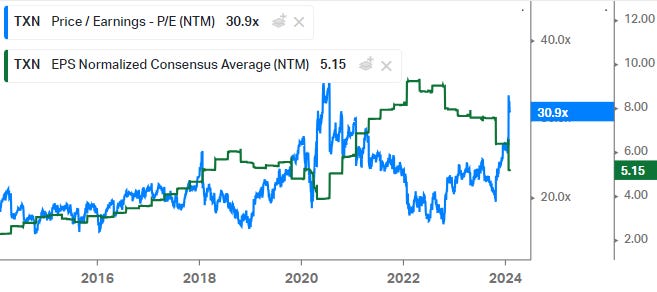

Looking at recent share price performance — which has held steady despite the downturn — it’s clear that these shares are being held by long term investors. The chart below illustrates these dynamics, despite forward EPS estimates going south (the green line) with the cyclical semi pullback, we saw a strong re-rating of the forward PE multiple (the blue line). So basically, investors are looking through the cycle and are unwilling to sell or downgrade the shares for what they are seeing as a temporary cyclical headwind for the company:

ADI is a bit cheaper than TI, trading on 18x ‘26 EPS with 5% expected FCF yield by then:

Also here investors are willing to look through the cycle, paying a higher multiple for what should be a temporary downturn in estimated EPS:

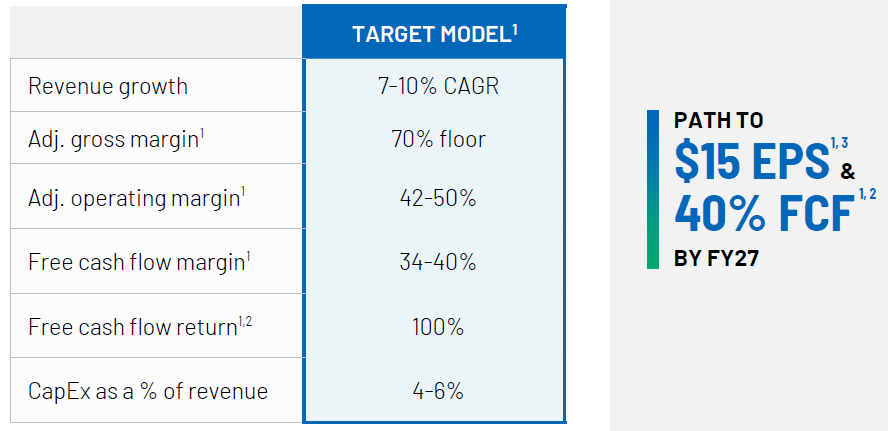

By 2027, ADI is targeting $15 of EPS, from their investor day:

The company’s CEO discussing this target at UBS:

“I think it’s reasonable. That’s predicated on being able to grow this business 7% to 10% per year. As I said, I think ‘24 could be a tough year but I think ‘25 and beyond, we’ll get back into a more normal growth pattern. So I still feel comfortable with all the growth vectors that we have.”

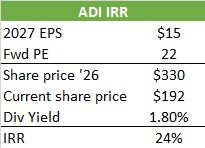

If ADI is right on this, investors could make a 24% IRR (annual return) in these shares, and I suspect one can build a similar model for TI.

So I actually like both names, I probably have a slight preference for TI as I like their 300mm strategy, which should bring a long term competitive advantage. Although I must say that ADI’s CEO has been making a solid impression as well, and on the positive their outsourcing strategy creates flexibility over the cycle. In my opinion, both companies have solid product portfolios and are probably among the best quality you can find in the mature-tech semi space.

If you enjoy research like this, hit the like and restack buttons, and subscribe if you haven’t done so yet. Also, please share a link to this post on social media or with others who might be interested, it will help the publication to grow.

I’m also regularly discussing tech and investments on my Twitter.

Disclaimer - This article is not a recommendation to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it can not be guaranteed that all information used is of this nature. The views expressed in this article may change over time without giving notice. The future performance of the mentioned securities remains uncertain, with both upside as well as downside scenarios possible.

Your arguments for a growing analog TAM with higher semi intensity is compelling for TXN and ADI. I also enjoyed your perspective on the Chinese analog competitors. ⭐✨

Would love to know your views on cultures on both companies as you correctly mentioned TI is a great marketing machine that leverage it's manufacturing advantage vs ADI more customer focused high end play. One point I heard while I was doing research on the names that TI has more aggressive old fashioned corporate culture for engineers vs ADI has more welcoming environment for it's people hence tends to see some talent churn over to ADI overtime from TI. Would love to know how you would think these difference could effect long term outlook?