Simulations Plus, Accelerating in Biosimulation

Simulations Plus, Accelerating in Biosimulation

An overview post a strong Q2

The main goal in biosimulation is to get an idea of how molecules such as drugs interact with cells, organs and the body as a whole. Drug development is not only complex, but it is also both capital and time intensive. The median cost of developing a new drug is now estimated to be around 1 to 2 billion dollars, with a timeline of going to market of around 10 to 15 years. Biosimulation software leverages mathematical models to predict how molecules behave in biological systems, resulting in lower costs for trials and getting to market faster. It does this by forecasting factors such as efficacy, toxicity and absorption for target molecules, allowing to screen for more candidates and to quickly arrive at the optimal dosage level. The alternative would be to arrive at these via expensive trials.

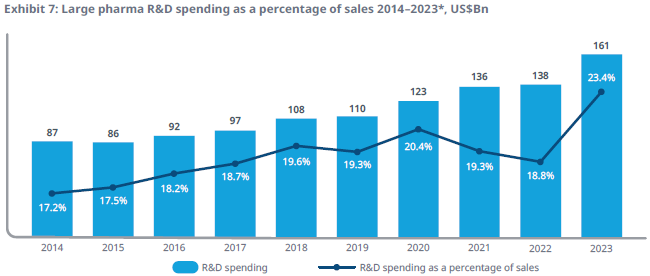

The chart below illustrates how large pharma R&D has been growing at a 7% rate. However, biotech is much more volatile, with booms and busts of R&D funding. According to Simulations Plus (SLP), the overall spend on drug development from large pharma and biotech combined would be around $200 billion per annum. Within that, biosimulation is a market of only $3 billion and is growing at an attractive annual rate of around 17%.

This is SLP’s CEO at the BoA conference in ‘21 discussing the challenges in drug development and how their software tools can improve outcomes:

“A number of 5,000 target drug molecules go into the development cycle for every 1 drug that is brought to market. The challenges are how does the drug work, is it safe, what's the right regimen, what is the biological effect and what are the risks or toxicity? Our products and services are focused on answering those questions, reducing the trial-and-error nature of the historical process. Modeling and simulation is a means by which you can get to an efficacy, safety and regulatory approval more efficiently.

We deliver very accurate drug and biological models to our clients, in the analysis from early discovery through to regulatory approval. We have a portfolio of software products, all of which are recognized as leading tools for model-informed and data-driven drug development. And we have a consulting practice that supports our clients from basic outsourcing needs to addressing more tricky issues in terms of simulation techniques.

Having started in the early days of adoption 25 years ago, we now have 250 clients and a high retention. Modeling and simulation is a combination of skill sets that runs the gamut from physics, chemistry, statistics and pharmacology. The number of scientists in this space that could run the engine and use the software was relatively low in the early days, it was a unique skill set but today, there's more than a dozen PhD programs in computational biology out there.

Scientific acceptance in the regulatory environment has been another factor. Over time, the FDA and their equivalents around the world began to utilize simulation internally in their evaluation of drug submissions. That built up to a FDA that today issues guidelines to the industry in support of modeling. When COVID hit, one of the first FDA guidelines to the industry was how modeling and simulation could be used to still maintain the value of clinical trials that were disrupted.

When the FDA issues for example a bioequivalence waiver, basically it waives the requirement to go into the clinic and perform a clinical trial to prove an efficacy or toxicity issue. That can be based on data and analytics brought to them through simulation. Obviously, the time and the cost of the clinical trial can be high, but the real big impact is getting that drug to market 6 months or a year earlier. Initiating the revenue stream for a drug can be quite dramatic for our clients.”

At the recent capital markets day, the company disclosed that the number of clients had risen to 400. Around 40% of SLP’s revenue mix stems from services which usually I’m less interested in as barriers to compete tend to be lower here. However, as these services are mostly helping clients with modelling and simulation in SLP’s tools, it’s really tied to the software business and there probably aren’t many competitors around which will have this know-how.

The number of scientific publications making use of biosimulation has been accelerating over the covid years:

SLP mentioned that over 1,300 publications cite their products and services contributions, so comparing these numbers to the data above would give them a market share of 16% in the overall space. Later on we’ll dive deeper into the competitive landscape.

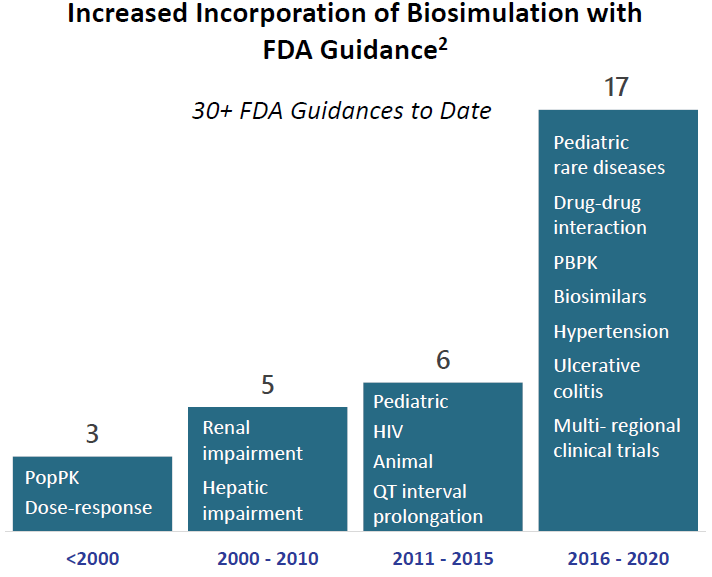

Also the FDA has been expanding guidance on where biosimulation tools can be incorporated:

Another new driver for adoption is a regulatory push to reduce testing of chemicals on animals, from the recent capital markets day:

“About 10% of our customer base today is in the non-pharmaceutical space, chemicals, cosmetics and consumer goods companies that have already been told by regulators around the world, especially Europe, that they need to greatly reduce or completely eliminate animal testing on some products. With the offerings that we have, you can start predicting without any animal data and with reasonable accuracy, what the absorption and exposure of chemicals systemically would be.”

Similar to the industrial CAD and simulation software markets, the biosimulation market utilizes a series of software tools specialized for each task. Gradually tools are now being integrated into software platforms, although the focus is also still on building out these tools with more advanced methodologies so that they can be cross-sold to clients. These then create a workflow from this series of tools. SLP’s CEO discussing this topic:

“We have several large entities that utilize the full suite of products and services but there are gaps. The industry itself is a very siloed process, with discovery and clinical departments. Modeling and simulation developed in its early days to provide solutions to these various departments in a sort of point effort. As modeling has become more strategic for our clients, they look more broadly at its use from start to finish. And that's been a focus on our part to develop a suite of platforms that can support the full scope of modeling needs. We’re very focused in terms of making these tools easier to use and more efficient, and that brings new companies into the fold as well.”

A number of these tools have been added to the portfolio by acquisition. This is SLP’s CEO discussing their M&A strategy:

“The strategy is broad and covers both the software as well as the service space, albeit our focus leans in the direction of the software side. This is evidenced by 2 of the 3 acquisitions to date having been software oriented and I would anticipate that to be the case going forward. Our focus on the software side is both in terms of expanding functionality that could be integrated into our existing platforms as well as acquiring other stand-alone solutions that address needs between what we provide today. There is a good population of companies out there, small privately funded entities that have developed solutions that would be great additions. We've been pretty strict in terms of our criteria for acquisitions, looking for product and culture fit, but also focusing on accretive acquisitions at a good valuation point.”

Simulations Plus’ software and services portfolio

Basically there are three key software tools, 60% of software revenues comes from GastroPlus, 16% comes from ADMET Predictor and another 16% from Monolix. The remainder are some smaller point tools.

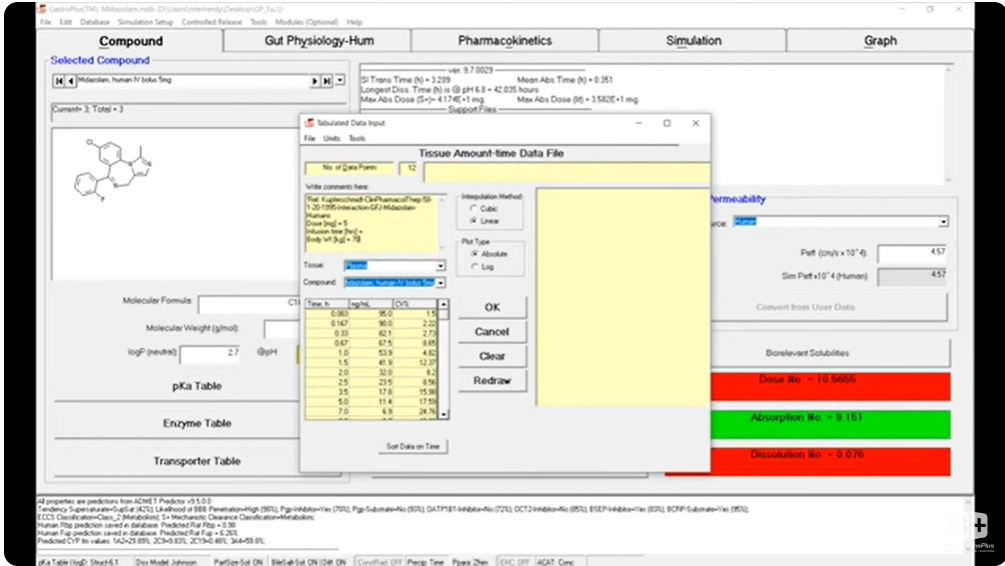

Gastroplus is currently the flagship and it can simulate how a drug will be absorbed and distributed into the bloodstream, how it will interact with tissues and organs, and ultimately how it will be removed. This helps researchers understand a drug’s bioavailability, dosing requirements and drug-drug interactions. A screenshot of a researcher using Gastroplus:

The company will also launch a new version of the software this year called GPX. SLP’s head of Cheminformatics discussing GPX at the capital markets day:

“The four areas of primary investment for GPX include model customization, software engineering, data management and deployment options. In addition, we are making investments in integrating more technologies, applying AI to provide expert coaching and support users on a real-time basis, building mechanistic delivery models all around the body for different molecule types to support small molecules, peptides and biologics, and providing true polypharmacy simulation capabilities to mimic a patient's real-world medication schedule and better assess things like drug-drug interactions. There are lots of different animals and human population groups in which we need to simulate and predict the exposure of drug, and I'm really happy to say that GastroPlus has been validated across it all. The feedback so far from those that have seen it and we've done lots of demos, is when can I get my hands on it? We have been very busy working on all of the ancillary documents and training materials, and myself and others are getting ready for a very busy travel season in 2024 as we go and visit with just about every company possible.”

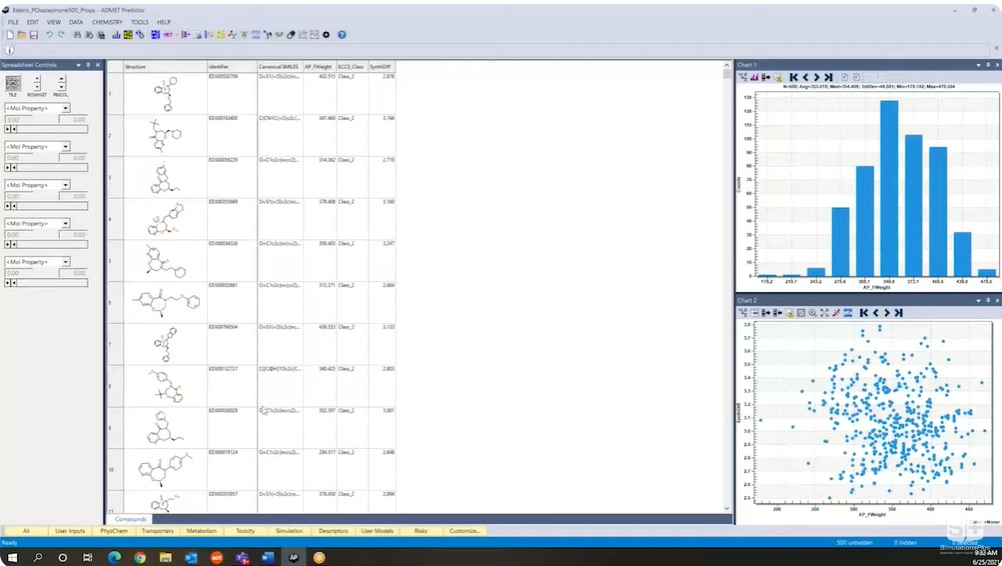

The second key software is ADMET Predictor, which uses AI to assess the properties of molecules. So researchers can use it to screen large amounts of potential molecules to narrow these down to the most promising candidates. Overall, the software can predict 175 molecule properties such as solubility, permeability, lipophilicity, how the molecule is metabolized in the liver, and potential mutagenicity. A screenshot of molecules being evaluated in ADMET Predictor:

ADMET can also be used to design new molecules and then optimize them by running them through GastroPlus. So combining these two tools can give a powerful workflow to find new drug candidates. And with AI methodologies only improving each year, this could be an interesting long term opportunity. The company also mentioned that they are receiving data from clients to train AI models. This is the company’s head of Cheminformatics on this topic:

“Our team successfully integrated the data that was provided by several large pharmaceutical and agrochemical companies to retrain our machine learning models. We also announced partnerships with the Institute of Medical Biology of the Polish Academy and the Sino-American Cancer Foundation, both are leveraging our expertise in AI to help with the discovery of novel molecules against 2 different emerging cancer targets. In addition, both collaborations provide for incremental benefits of joint compound ownership or milestone payments if successful. Molecules have been selected for synthesis, and we are very excited for the first round of experimental results that should be coming within the next 2 to 3 months.”

So he mentions two interesting points. As we know, the predictive power of an AI model is mostly a function of both the quality and quantity of data that goes into it during training. At several events the company has mentioned that clients are sharing data with them, so this should create a strong moat and network effect among the few software players in this field as they will be able to provide the best AI models. Additionally, software tends to be sticky in general, and as PhDs are highly trained on SLP’s products, this should remain an attractive business to own. The second interesting point is the mention of joint ownership, with additional revenues coming in should these molecules hit certain milestones. So we’re basically getting free optionality if novel molecules turn out to be a success. What would be really be great is if in the future a certain royalty percentage can be secured. This would start bringing in substantial revenues should a molecule become a $1 billion-plus drug.

This is SLP’s CEO discussing the impact of AI on the biosimulation market:

“As AI technologies continue to develop, we keep pace by improving our use of AI technology to enhance our modeling and simulation solutions. Additionally, AI accuracy is only as good as the datasets used for training and our access to accurate public and private data is a true competitive edge in our business. Our long-standing partnerships and collaborations with both industry leaders and regulatory agencies have granted us significant access to both private and public data, essential for perfecting and refining predictive algorithms. Our business rooted in both science and data stands to meaningfully benefit from evolving AI applications.”

The third key software is Monolix, which uses advanced statistical techniques to understand how drug effects vary between individuals in a population. Additionally, it is used to simulate various dosing and trial designs, helping to increase success rates. More recently the software has started to leverage biomarker data to better predict oncology treatment outcomes. Oncology (cancer) remains the largest therapeutic research area so obviously this can be an interesting growth driver in the coming years.

This is SLP’s head of Pharmacometrics discussing Monolix:

“Pharmacodynamic models describe the positive or negative effects the drug has on a patient and elucidates the relationships between dosing, individual patients and outcomes. Our models are used to select the right dose at the right time to achieve optimal therapeutic outcomes. Our product is the Monolix suite and is designed to save time and energy for pharmacometricians and biostatisticians.”

An example of data analysis being carried out in Monolix:

The services business is actually fairly interesting as well, although it is lower margin than software. This is SLP’s head of QSP services discussing some interesting examples of how they’ve helped clients:

“First example of a success story. Our client submitted results to the FDA that resulted in the removal of one of the requested dosing levels within the Phase III study, saving the company many millions of dollars. Next, we'll talk about Biohaven. This company had the CGRP program, a set of compounds focused on treating migraines, where they were predicted to be safe by our safety platform despite historical liver toxicities from other drug candidates in the same space that focused on this target. The company moved forward with confidence and they showed safety in their trials. They received FDA approval and were subsequently sold to Pfizer for $11.6 billion.

Next, Cenicriviroc, which is a therapeutic candidate for liver disease and which was taken into a very expensive Phase III study where it failed to show efficacy. Our tools could clearly predict the mechanism of action and that in this case, it would not be effective.

Lastly, there's an exciting recent example around the compound Fezolinetant. This was a recently FDA approved drug which promises to be a $1 billion seller for the company, Astellas. It progressed to approval after our liver safety platform helped successfully pick the Phase III dose range of 30 to 45 milligrams, despite liver issues at much higher doses.”

So now that we understand the tools, we can have a deeper look at the competitive environment. This is SLP’s CEO discussing their competitors:

“Certara comes up frequently in the biosimulation market, which is just a portion of their business as they've expanded over the years into other areas such as regulatory writing for example, a space that we don't focus on. We're very focused in terms of biosimulation tools and services. But in that space, there's some competition between our GastroPlus product and their Simcyp product. Typically our clients will utilize both. I think ours is considered the sort of workhorse engine, and the majority of needs are filled by GastroPlus. And there's some functionality, some therapeutic areas in which the insights that can come from Simcyp are appreciated. But I think ours is the largest platform in terms of customer count.

ADMET Predictor supports the lead optimization process and discovery, there’s not really any strong competitor out there for that 2D predictive capability, that can take a molecule and provide predictive information across 150 different characteristics. Schrödinger has a tremendous 3D tool that is complementary but it's not competitive with ADMET Predictor. So a client will typically use both tools in their lead optimization process.

Monolix is our pharmacometric tool. Its primary competitor is NONMEM, an application that was really one of the first products in modeling and simulation 25 years ago out of UCSF. And it still is in the market but Monolix has the modern front-end, the modern technological architecture. And we are doing well in terms of taking market share in that space. We are the up and coming, fast-growing alternative to the old product in that space.

On the consulting side, we and Certara are the 2 largest providers of services in this space. Then there are a number of one scientist to 20 to 50 people sized organizations out there.”

Long term there is a strong opportunity to grow outside of the US, which currently still contributes 70% to SLP’s revenues. This is the CEO discussing their geographic strategy:

“Our number of consultants we have on the ground in Europe and Asia is too few for us to participate as strong as we should in those areas. I see that as a tremendous opportunity to add to the growth of the company going forward as we expand our reach into those 2 territories. Drug development on a worldwide basis, the majority is in North America, so there will always be that 60-20-20 split. But there are probably accelerated growth opportunities for us as we improve our presence in those 2 markets.”

A new upcycle

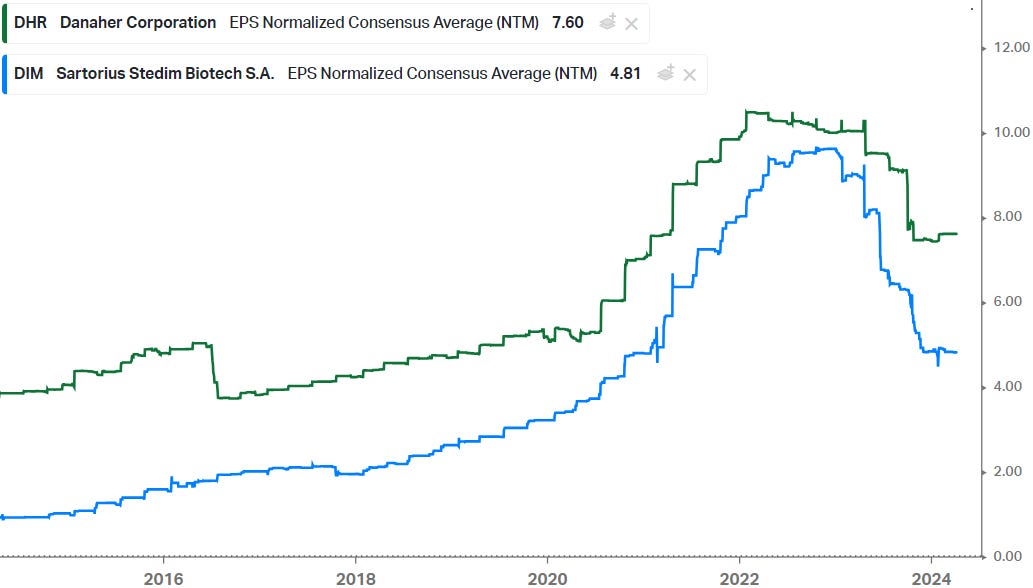

After the covid biotech boom, the space went into a major downturn. This can easily be observed in forward EPS estimates for picks-and-shovels suppliers to the industry such as Danaher and Sartorius Stedim (chart below). However, it also seems that estimate revisions have started bottoming out now and that we’re moving along the trough.

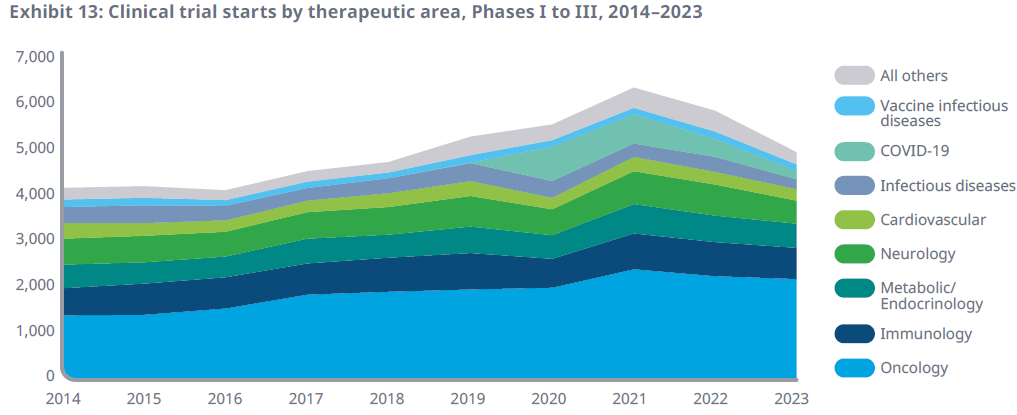

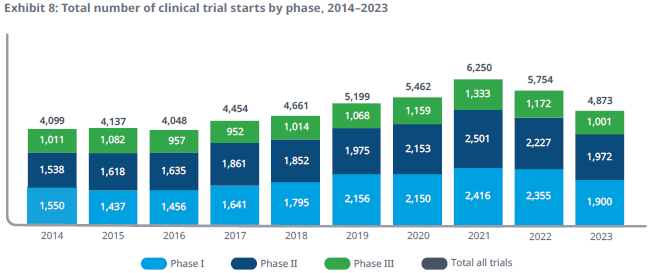

We can also see the cyclical correction in the number of clinical trials being carried out:

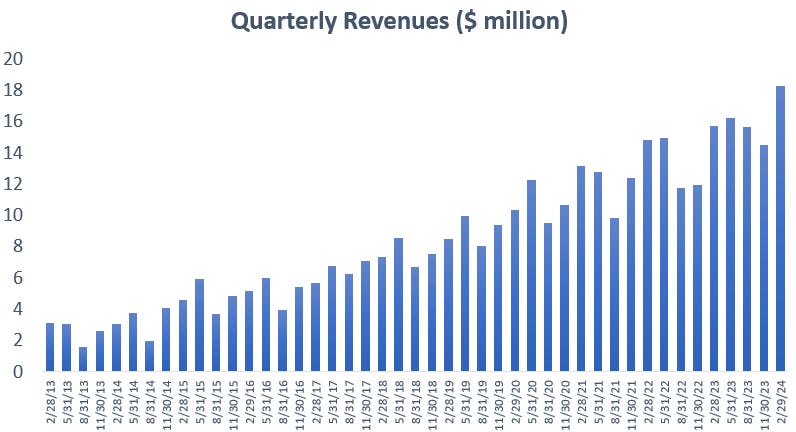

Due to these headwinds, SLP’s quarterly revenues had been flattish over the last two years, but that changed last quarter with a whopping 26% quarter on quarter growth rate:

You can also see that despite the long term upwards trend in quarterly revenues, there remains a certain amount of non-seasonal volatility. There are two factors at play here. One, the company’s revenues get a high contribution from services of around 40%, which can be cyclical. Two, the company also mainly still sells perpetual software licenses, resulting in more lumpy revenues compared to the more modern subscription model.

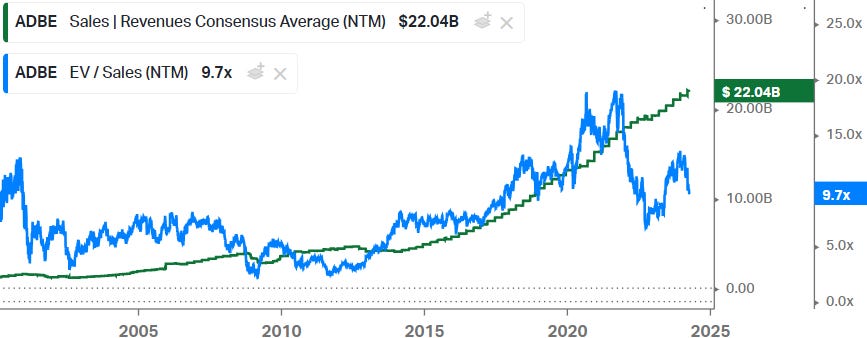

The latter is actually an opportunity for long term investors in the stock, as when they decide to transition to the recurring and higher revenues that the subscription model provides, shareholders will be rewarded. A good example here is Adobe, as they transitioned to the subscription model over the 2014-2015 period, investors were rewarded with less cyclical and higher revenues in the subsequent years, resulting in a higher sales multiple:

This SLP’s CEO commenting on the overall market environment during the Q2 call:

“Our market continues to show encouraging signs of strength. In the first calendar quarter of 2024, biotech funding has been strong. Especially for companies that have drug candidates in the clinic. For large pharmaceutical companies, funding continues to vary depending on their drug program and business outlook, but the overall market is healthier compared to a year ago. For the balance of 2024, we remain cautiously optimistic that demand for our comprehensive suite of products and services will continue to gain momentum.

On the pharma side, circumstances are more related to the individual company, i.e. their outlook in terms of patent exposures on revenue streams on their new programs. You've got a wide range of scenarios, from Novo Nordisk at one extreme and other companies like Pfizer that have announced significant cutbacks this year. So mostly everyone is in between those 2 streams. But there's still a lot of churn, cautiousness and sorting out of drug programs, which are going to be invested in and which not.

On the biotech side, it's anecdotal depending on where their drug candidates are in terms of the cycle and when they get the funding. Typical sales cycles in our industry can range from ‘I need a new seat and I need it tomorrow because I just hired somebody’ to prolonged budgetary activity. But certainly, within the first quarter of funding activity, you're not going to see a quick turn in terms of market volume. But in the 6 to 9 months range, I would anticipate many of these companies that are getting funded, are going to be advancing their candidates. Probably the biggest impact is as funding goes into the biotech companies, they hire people from large pharma that are pre-existing SLP product users and that creates an opportunity quickly in terms of sales cycles.”

Some highlights from the same call on customers buying software licenses:

“This past quarter, we had yet another large pharma company that made the commitment to displace entirely the competitive product and go 100% to the use of Monolix for their needs there. Monolix is doing quite well, since our acquisition of that product line in 2020, it has been our fastest-growing software platform, displacing the incumbent leading market share product.

Yet another AI startup biotech company licensed our ADMET Predictor tool to supplement what they are building separately. I think that endorses that we're not being displaced in terms of many of these AI technology builds and it shows the value of what we've built and brought to the market.”

Financials — share price of $46.7 at time of writing, ticker SLP on the Nasdaq

Historically, the business has been growing at a 20% revenue CAGR including some smaller acquisitions. However, as margins have come down due to the growth in services and SBC, the EPS CAGR stands only at 12%. SBC remains limited at $4.8 million over the last year, which is less than 0.5% of the current market cap. Software is very cash generative as contracts get paid upfront, so the FCF margins are 36% and have been growing at a 29% CAGR. Additionally, the company has a net cash position of $108 million on the balance sheet. So obviously the financial profile is very healthy here.

Over the last 10 years, a huge market rotation has occurred with institutional money shifting into quality-growth type companies. Typically investors appreciate companies which can generate durable growth combined with a strong moat to protect the cash streams from competition. So whereas you could buy a stock like this for 5 to 6x sales 8 years ago, names like this now typically trade above 10x sales as we’ll see below. However, looking at the more recent trading history since 2018, the multiple is now towards the lower end of the range:

This is not a phenomenon unique to tech, you used to be able to buy a company like Costco at 20 to 25x PE, but now you’re paying 43x. While these are all great companies, I do think that multiples for quality-growth type stocks are looking somewhat stretched here, and I suspect we won’t see additional further re-rating from here. Which would mean that investors can still capture the EPS growth and dividends in these types of names, resulting in positive returns as long as these kind of multiples hold. The main risk here is inflation picking up again, which puts pressure on stock multiples and can cause a market rotation into commodities and other value-type stocks.

Compared to the rest of the CAD and simulation space, SLP is valued in line on an EV to Sales basis but does have a higher weighting to lower margin services, so it is now the most highly valued name on a PE basis together with Altair, which is another name active in simulation. These companies are typical takeover targets however, as we saw with Ansys just a few months ago, so somewhat of a premium is probably justified here. I also do think that SLP has one of the best runways for long term growth in this space, making again a certain premium justified. If you’re looking for value in CAD, Autodesk and Dassault are good candidates, you can still buy them at 30x PE..

.. which are multiples closer to long term historical trading ranges. For example, in the case of Dassault Systemes:

If you’re looking for names which can accelerate growth with the use of AI, I suspect names like Cadence, Synopsys and SLP will be the better plays.

Wall Street’s estimates below, the stock is now trading on 50x ‘25 PE, so obviously valuation is looking quite full here in my opinion. As we saw above, quarterly revenues tend to be quite lumpy with the signing of licenses, so sooner or later you will get a disappointing quarter and that’s usually a good time to pick up a stock like this.

If you enjoy research like this, hit the like & restack buttons, and subscribe if you haven’t done so yet. Also, please share a link to this post on social media or with others who might be interested, it will help the newsletter to grow, which is a good incentive to publish more.

I’m also regularly discussing tech and investments on my Twitter.

Disclaimer - This article is not a recommendation to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it can not be guaranteed that all information used is of this nature. Before making any investment, it is recommended to do your own due diligence.