Silicon Labs vs Nordic Semi, the battle for the IoT semiconductor market

Silicon Labs vs Nordic Semi, the battle for the IoT semiconductor market

An overview of the space

IoT, the world of connected devices, remains an interesting area for investment exposure. One, this is a market which has been growing at double digit rates over the last decade and is forecasted to continue to do so. Two, there are a number of larger semi players in this field and customers use their provided software tools to integrate and customize IoT SoCs (System on a Chip) into their products. So not only do these SoC designs regularly have to be updated for the latest wireless tech, but customers are also trained on the software, strengthening the moat for these players. Three, provided SoCs are becoming more complex, advanced and integrated, lifting ASPs over time. Finally, we should be nearing the bottom of the semi cycle now in this market, so investors have the prospect of a strong growth recovery once the cycle turns.

IoT Analytics provides an overview of the number of connected devices in the world measured in billions. Usually these devices are connected to local or personal area networks, but also cellular is becoming an interesting growth market:

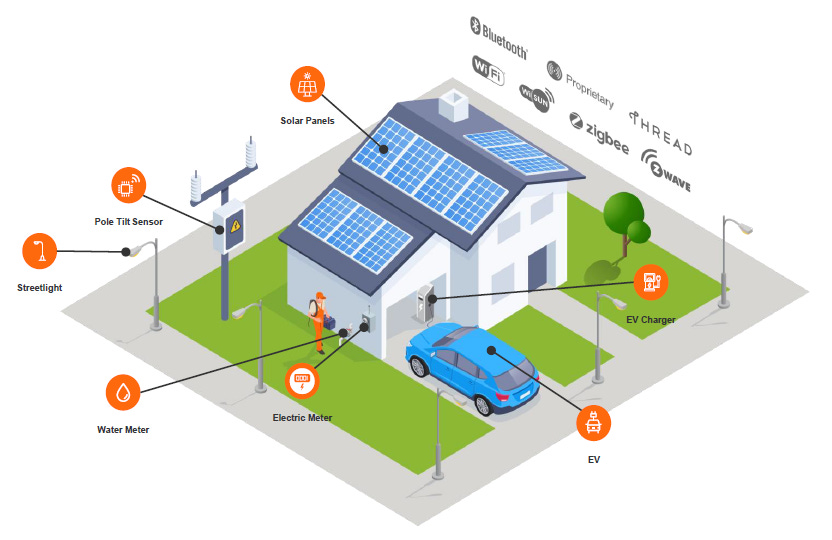

Silicon Labs (SiLabs) provides some typical examples of where these SoCs can be installed, from water and electric meters sending back data, to solar panels, street lighting and EV chargers. There are a wide variety of wireless technologies to connect these devices but the best known ones are Bluetooth for short range, WiFi for mid range and cellular for long range.

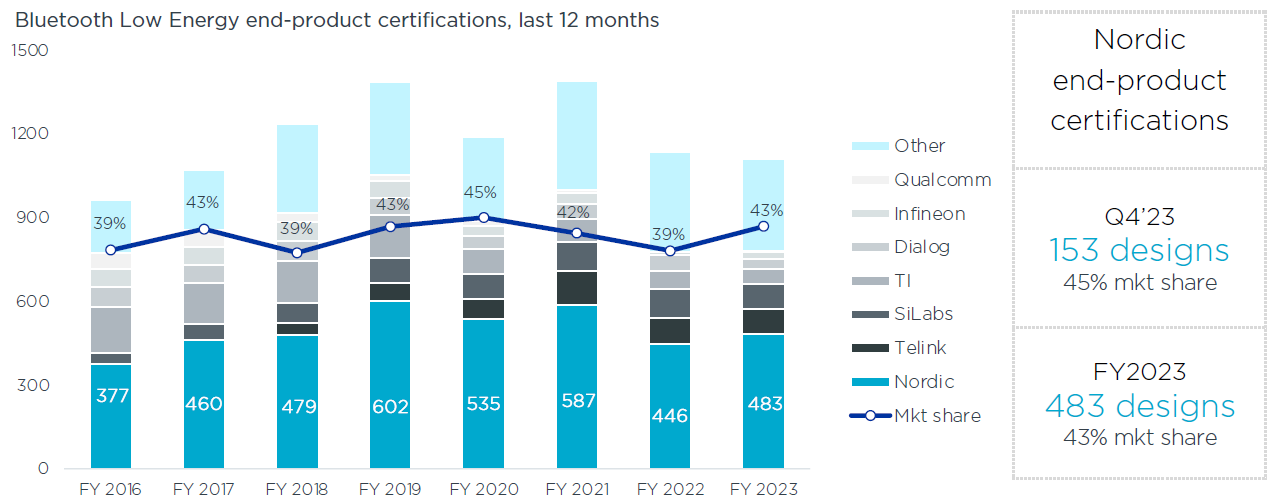

Nordic Semi is extremely strong in Bluetooth Low Energy (BLE) with a 43% market share as seen on the number of design wins below. BLE is used for very low power and short range data transmissions, for example to send data from your smartwatch to your smartphone. Some other uses include tracking where your cat is going, or to receive data from medical devices such as a glucose monitor. We can also see on the chart below that SiLabs has been winning some share as well as Telink, a Chinese player which I suspect has mostly been winning designs in the Chinese market. That said, Nordic retains a fairly attractive share of around 43%.

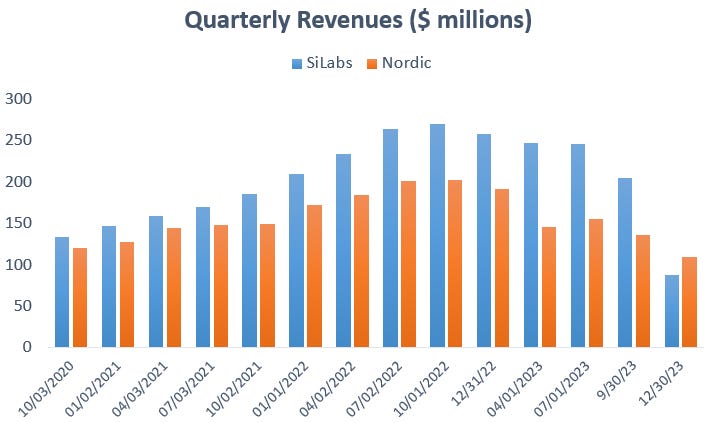

In the overall IoT market, SiLabs has been achieving stronger growth over the previous years, albeit it also entered a stronger cyclical correction more recently:

Whereas Nordic is very strong in BLE, SiLabs is the strong player in multi-protocol SoCs. This is their CEO giving an introduction to the company:

“We're the largest in the world of what we do and the easy way to think about a wireless SoC, you have on one chip the wireless capability, the general purpose compute, machine learning, power management and security. On top of that, we provide all the requisite software and customer support across multiple wireless technologies. We're one of the only companies in the world that has all the requisite wireless technologies, and we know how to make them work well together. Our end market is growing outside of the cycle around 15% annually and our goal is to always be gaining share within that space, which we've done over the last decade consistently, giving at least 20% growth. And the companies that have this as a side show, it doesn't give our customers confidence that it might not be their core priority as a company. And that's what we saw during the supply crisis, a lot of the bigger companies retrenched and allocated supply elsewhere, this really spooked our customer base.”

Nordic has been busy replicating this strategy by also offering multi-protocol SoCs including low power cellular, which SiLabs has decided to stay out of for now. Both companies make use of a platform approach, where they will only release a limited number of SoC designs, which clients then can adapt via the provided software tools. This strongly reduces inventory risks as the demand for these chips is broad-based, which mitigates the obsolescence risk which you can get with highly customized semis e.g. ASICs.

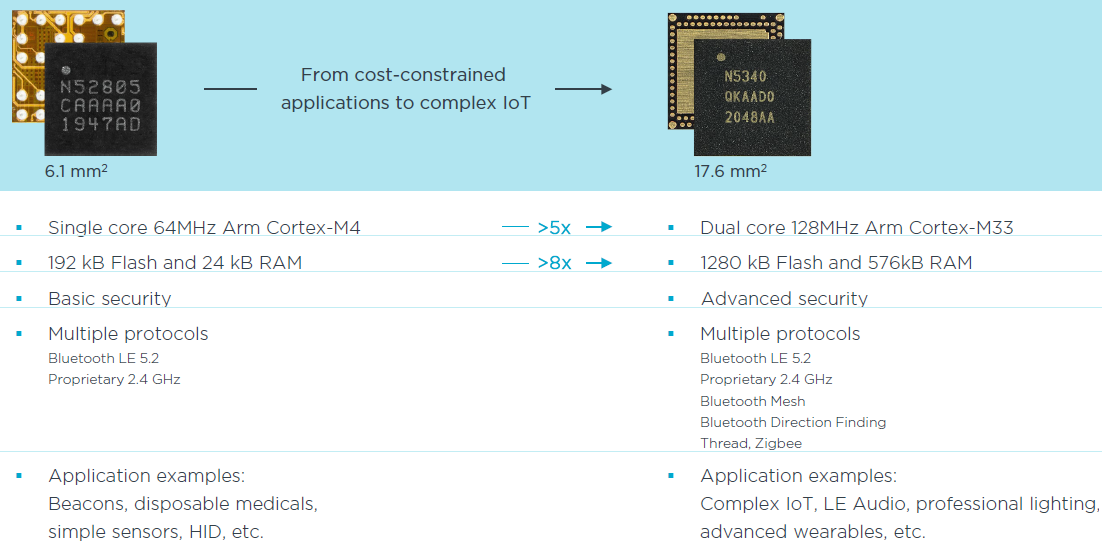

Two examples of Nordic SoCs are shown below, the smaller one is aimed at BLE while the other offers a wider variety of protocols:

Both manufacturers have been launching single and multi-protocol SoCs to address a wide variety of use cases. In addition, both are adding advanced features such as low power AI accelerators and cryptographic security while at the same time both are developing more completely integrated systems, for example by also including power management. So besides the high future volume growth of the IoT market, there is an additional opportunity to increase ASPs, as both SiLabs and Nordic are providing more complete and advanced integrated systems.

SiLabs goes all in on IoT

SiLabs didn’t use to be an IoT specialist, the company had an automotive and an infrastructure semi business, as well as one for handset and PC semis a long time ago. However, when they saw the opportunity arising in IoT, the company decided to divest their other businesses to SkyWorks for $2.75 billion and go all in on IoT. This the previous CEO discussing this move in ‘21:

“We just announced the divestiture of our infrastructure and automotive businesses to Skyworks back in April and that allows us to focus as a pure play on the Internet of Things, which is just a massive opportunity sitting in front of us. It's a $10 billion SAM that we're targeting, lots of runway for revenue growth.

The founding of the company was really around mixed-signal and RF integration and so we did a number of hit products. We took the company public in 2000 and went after the PC and handset markets. We got a 50% share in modems, got 25% share in mobile handsets and those really propelled the company's first wave of growth. We did a number of other products, but we ended up divesting our handset business in 2007.

We sat down and said, we've got these great capabilities, we've had lots of successes in multiple markets, but where are semiconductors going for the next one and two decades. And we saw that the connectivity that's going into PCs and handsets is now going to get really embedded into everything. And we said the integration of wireless connectivity and building SoCs for all these embedded devices is going to be a huge opportunity. We've done a number of acquisitions around this to bring in talent and capabilities, so now it's not just mixed-signal, it's also communication protocol stacks, networking, tools and collecting data. We've grown that business from about $100 million to what will be about $650 million this year and there's a lot of room ahead. You look back at the PC industry and Intel dominated that, you look at the mobile industry and Qualcomm came out ahead, I think that we've got the opportunity in IoT to become the market leader.

There are a lot of wireless protocols that are necessary in IoT, you'll use Bluetooth to talk to a handset, but then you'll connect to a mesh network with Zigbee or Thread, or you'll connect to a WiFi network. And there's a lot of proprietary networks that are supported as well. Between devices, whether it's Google, Amazon, Comcast or Apple, a lot of contributors are rolling out Thread mesh networking, so these devices can communicate with each other at the gateway or at the device level. We've designed our platform to really support all of these protocols in a holistic way and update those over time. And doing that across thousands of different applications and tens of thousands of customers takes a lot of focus. It requires a different approach than just having a microcontroller with connectivity. We're on our fifth generation of development tools and this helps our customers get to market faster. Some customers are experts at wireless, and others are just learning and need a turnkey solution.

Cellular by comparison, can cost 10x more and have a fraction of the battery life. So low-power wireless allows for more than 10x battery life at a fraction of the cost. It opens up the door to so many applications that otherwise couldn't utilize wireless technology. The bulk of the market will be driven by low power, and that's where we are incredibly well positioned.

Security is essential, people have to trust these devices. You've got to embed payment grade security hardware and software into these devices. We're integrating very sophisticated accelerators for security algorithms onto the chip so that you can't hack it. The other important thing is that the hardware is energy optimized. A lot of these applications are running off of batteries, 10 year batteries and so you've got to minimize the amount of data that you're transferring. On top of that, we’re integrating machine learning algorithms. When you have sensor data coming in, you've got to have some intelligence to only transmit when you see something that matters.”

The semi cycle and SiLabs’ whopping current pipeline

So the IoT semi cycle has been brutal as we saw in the quarterly revenues chart above. A large factor here currently is that both distributors and end-customers have been reducing inventories, so currently both SiLabs and Nordic are selling less than the number of IoT semis being shipped by their end customers. However, SiLabs is now calling for their revenues to have reached a bottom, in what was really a disastrous Q4. Basically, they are seeing a new upcycle starting due to the strong number of designs they’ve been winning. This is the company’s CEO at the recent Morgan Stanley conference:

“This is the first time we went through anything this severe. Multiple learnings from this. We learned that we weren't carrying enough die bank during the upcycle and we learned that we need mechanisms to track end customer inventory. We went out in Q4 and said, look we're not calling the market bottom but we are calling our bottom as we can grow sequentially from here. We know that our consumption is well above our revenue level as people work down inventory. And we've won a tremendous amount of designs over the last few years that are just starting to come to fruition now. So you put these two together, we don't need the market to recover to drive sequential growth, but the market will recover at some point and that will give us an additional lift.

We built up internal inventory intentionally, we have no contractual obligations to do so but that was just a learning from this cycle. We need to give our customers confidence with all these design wins that we can support them as they ramp. Our channel inventory is the lowest it's been in the last three or four years, it’s actually lower than it was during the supply chain crisis. I'd be worried if we didn't have the internal die bank to give us the ability to respond on the other side. End customer inventory is still high. In Q4, we said that our customers are carrying an excess of a quarter than what they should. And they’re still working it down in Q1. Everyone wants to know what the actual consumption is right now and it's not precise, but we know it's over $160 million a quarter (SiLabs did $87 million in revenues last quarter).

Like-for-like pricing has been pretty stable. In our space, price discoveries happen at the design win phase, very rarely will we move pricing once it's up and running. In the last call, we did talk about one competitor who is maybe acting a little bit unusual on price at this point in the cycle but they have very little overlap to us, we're really just trying to give a fair picture of what we see out there. But the reality is pricing is pretty inelastic.

In Industrial & Commercial, we started to see the correction in Q2 of 2023. We are now seeing bookings improve consistently over multiple months and we're starting to see the discontinuation of pushout requests. We're seeing now pull-in requests and that's encouraging.

In Home & Life, we're just starting to see the impact of those design wins ramping now. Like the India smart metering rollout, Samsung for smart TVs, Dexcom for continuous glucose monitoring, and one of the largest two EV makers in the world is ramping our products in '24. Those are all happening kind of in this quarter to next quarter.”

At the same conference, the CEO mentioned they have a $18 billion pipeline. Assuming an average lifetime of 6 years would work out to $3 billion of annual revenues. For comparison, the company did only $780 million in revenues last year so obviously there is a strong prospect for high revenue growth in the coming years.

Nordic Semi on the other hand is not calling revenues to bottom just yet, this is their new CEO on the recent call:

“The current cyclical downturn has been more severe and more prolonged than anticipated and visibility continues to be low. We see continued inventory adjustments into Q1. During the fourth quarter, distribution inventories of Nordic components has definitely decreased but given the situation, we also expect distributors to further reduce levels during Q1. In relation to end customer inventory, it's really a mixed bag. Some have more than they need and others are saying that they're in balance.”

Moving into new technologies

We saw above that SiLabs has gradually been taking some share in BLE. This is their CEO discussing those and their move into WiFi:

“Our market leadership positions in IoT are getting pulled in by some of the biggest companies in the world. I'd also say technology-wise, we put our focus on Bluetooth 3 to 4 years ago and made huge progress there. We are unequivocally gaining share and taking chunks out of competitors like Nordic who was up on stage earlier. And we see that continuing in the next few years. In WiFi, we like the progress we're making. We just released our first product based on our combined technology that brings WiFi 6 with 45% to 50% less power consumption than any competing alternative. That means you change your batteries way less often.”

Larger companies active in WiFi IoT include Qualcomm, Broadcom, Texas Instruments and NXP. Also Nordic is moving into WiFi and the company sees their combination of a platform comprising Bluetooth, WiFi and Cellular as a unique selling point within IoT. This is the previous CEO discussing their strategy:

“We started with WiFi because this was one of the most asked about features among our customer base. It is a new technology to Nordic, and we come in where there are established players. So we’re bringing it into the Nordic platform and we see a lot of our customers that are needing WiFi and cellular. So there was a real opportunity, and when we made the acquisition of the assets and the teams. Nordic now has the ability to make a complete module, by mixing and matching these different technologies.”

Note that cellular is still an extremely small business for Nordic, while WiFi still has to start as well really, so currently Nordic remains largely a BLE and ASICs business:

Similar to SiLabs, Nordic has been acquiring semi design teams with the necessary expertise around the globe to enter these new segments. Of Nordic’s current employees, 77% now work in R&D. Obviously there is a lot of wireless know-how in Finland arising from Nokia’s historically strong position in this field and Nordic Semi has been adding some of these teams to their business. They also integrated more recently the WiFi team of Imagination Technologies and have been building out their design capabilities in India.

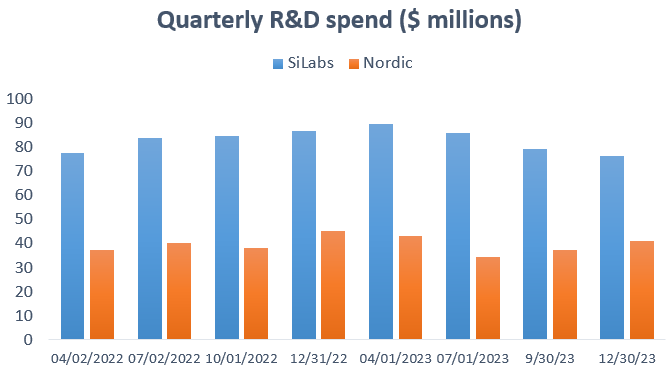

This strategy also highlights that it won’t be easy for newcomers to enter this field. The necessary skillsets aren’t easy to find while the field is also highly R&D intensive. SiLabs spent $330 million on R&D in the last year alone, or 42% of their revenues, while Nordic invested $155 million at a ratio of 29% of their revenues. Clearly these are budgets which won’t be easily available to smaller players or startups in the field.

A software moat

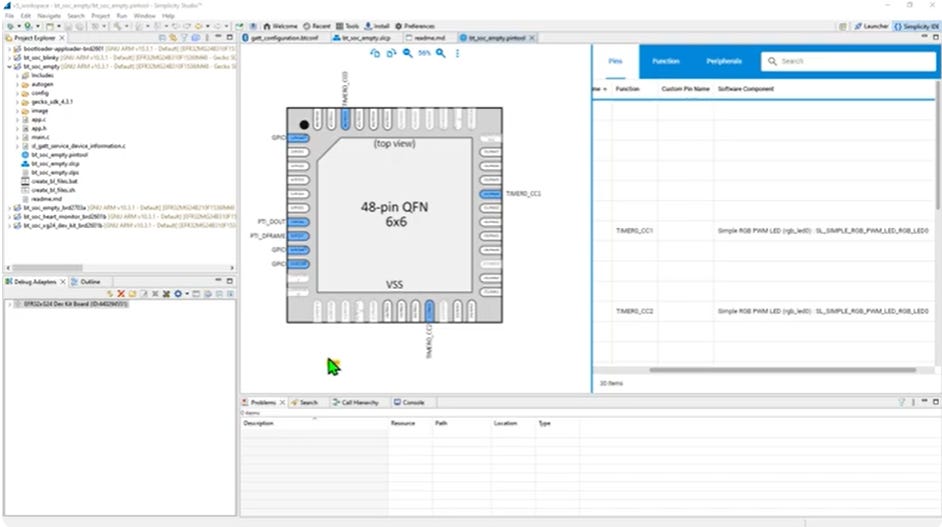

To get a feel for SiLabs’ and Nordic’s software moats, we’ll be taking a brief tour of their software studios. The main idea is that IoT engineers have a workflow set up to customize their SoCs. For example, this is how you can edit the code running on a Silabs chip with the company’s Simplicity Studio:

The composition of a SiLabs SoC is illustrated below. The core CPU is an ARM Cortex and then a rich set of peripherals are added from communication to analog and security.

By making API calls to the SoC, you can connect other microcontrollers:

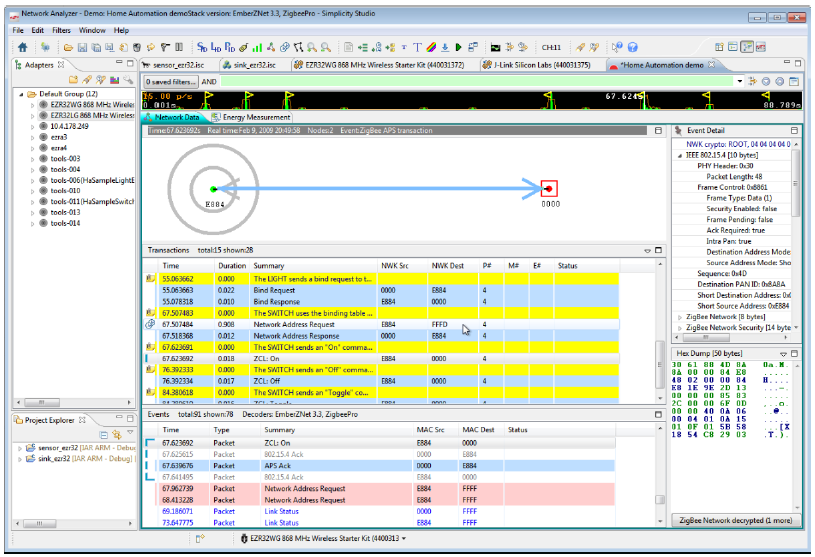

The software can then also be used to analyze the network traffic:

And to analyze power consumption:

This is probably just the tip of the iceberg but it shows how engineers use the company’s tools. Nordic has been building out similar tools and has also been integrating these into Visual Studio Code (VSC), which is by far the most popular coding environment and is open sourced by Microsoft. As a side note, Microsoft has become extremely developer friendly under the stewardship of Satya Nadella, you can even now run a Linux Ubuntu VM on a Windows desktop. And open sourcing VSC and acquiring the popular code sharing platform GitHub are just a few examples of this new direction. Integrating Nordic’s tools with VSC will definitely support the stickiness of the business in the IoT engineering community. The below image shows an engineer customizing his Nordic development board from VSC:

Financials - SiLabs current share price of $126 at time of writing, Nordic share price of NOK 94 ($8.64)

I like the set-up in Nordic’s shares currently, we should be nearing trough revenues while the shares are trading close to a trough multiple:

I do think that this is a good company and that their position in BLE should be defensible, so the valuation is looking undemanding here. It is also possible that they can leverage their strong existing customer base to grow in additional wireless protocols, making the long term outlook to be attractive here. The company also has a new CEO and he took questions at the recent conf call:

“My focus is on returning to growth and to restore profitability. An overarching key element will be how we prioritize our projects and resources for the short and the long term. We have extremely solid customers and Nordic has some really great products in the pipeline. We believe that these products will drive the next level of performance in the IoT markets and we are really excited about our first customer feedback on the 54 Series SoCs.”

Both Nordic and SiLabs will be launching a new 22nm SoC in the near future which look to be state of the art when it comes to IoT.

Nordic has somewhat lower margins than SiLabs as illustrated in the chart below. Basically Bluetooth has lower gross margins than the multi-protocol strategy which SiLabs has been pursuing.

Analyst estimates in USD for Nordic below, the company will clearly have to work its way back to $0.5 of EPS and then the shares are trading on an attractive 16x PE for what should be a good growth story.

Originally the company was targeting $1 billion in revenues by 2023 and at least $2 billion by 2026, this is back from the investor day in ‘21:

From the same investor day, the long term targets for EBITDA margins are at 25% as the company should get good leverage over time on R&D spend:

Cellular remains a very small part of Nordic’s business and currently 11% of revenues are being invested in cellular R&D. So if this business disappoints in the coming 18 months or so, this would provide an easy avenue for cost cuts and return to +10% EBITDA margins.

The other difference with SiLabs is that Nordic is much more heavily skewed towards consumer products at 62% of revenues, whereas SiLabs has more than 50% of revenues coming from industrials. Industrials is a more attractive end-market as the product lifecycles are much longer here, typically 10 to 15 years versus 2 to 3 years in consumer. So once you get designed in into an industrial product, the semi company get a long stream of revenues.

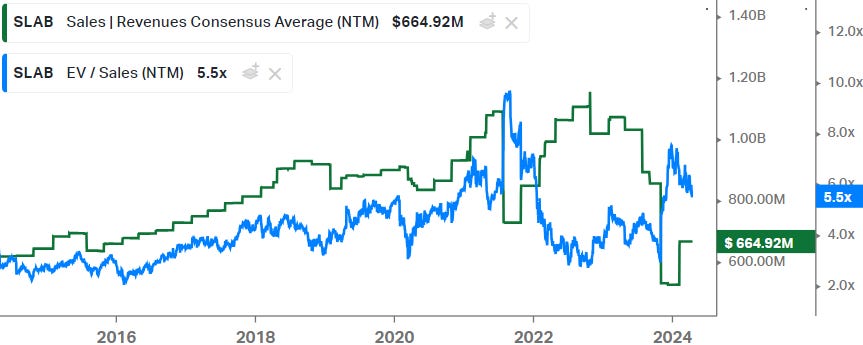

Let’s turn our attention to SiLabs now. After the company resetted expectations in Q4, the EV to Sales multiple has re-rated to 5.5x on what should be trough revenues:

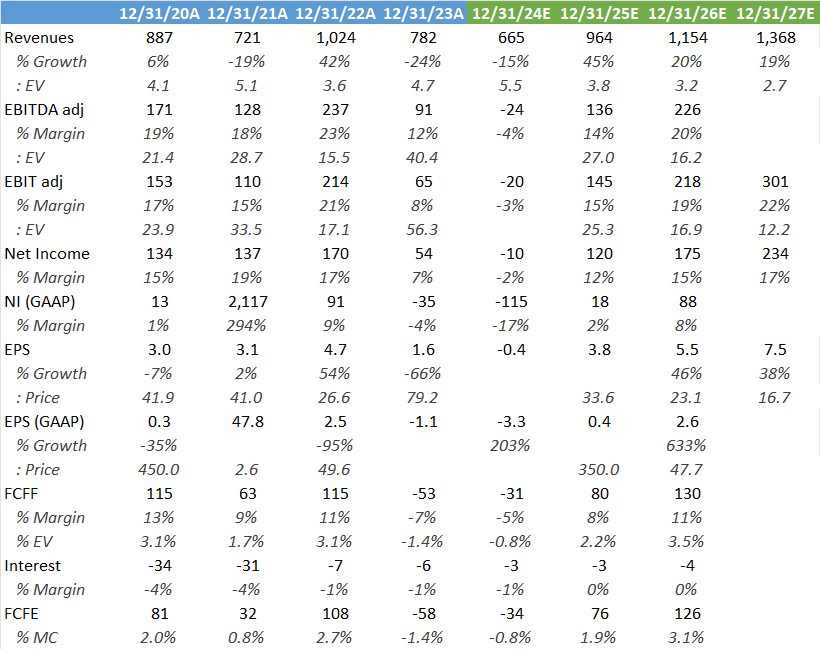

High growth will have to kick in during the coming years to justify this valuation, on consensus numbers the multiple will fall to 23x PE in ‘26 with a 3.5% FCF yield:

The last quarter was brutal for SiLabs and the company has responded with cutting costs. The company’s CEO discussed these at a recent conference:

“As we got to Q3 of last year, we executed what we anticipated to be just temporary reductions. There were executive team pay cuts, we shut off the bonus plan, shut down travel and really slowed the pace of hiring to just a bare minimum. As we started seeing how Q4 was taking shape, we had to convert a lot of that to structural changes. So we had the 10% reduction in workforce, the biggest cuts that we've ever done. This was really painful but necessary and it recalibrated our cost structure. As we look ahead in '24, we're going to start to open up spending a little bit but it's going to be calibrated to the pace of the recovery.”

Long term the company is targeting mid-20s percent EBIT margins:

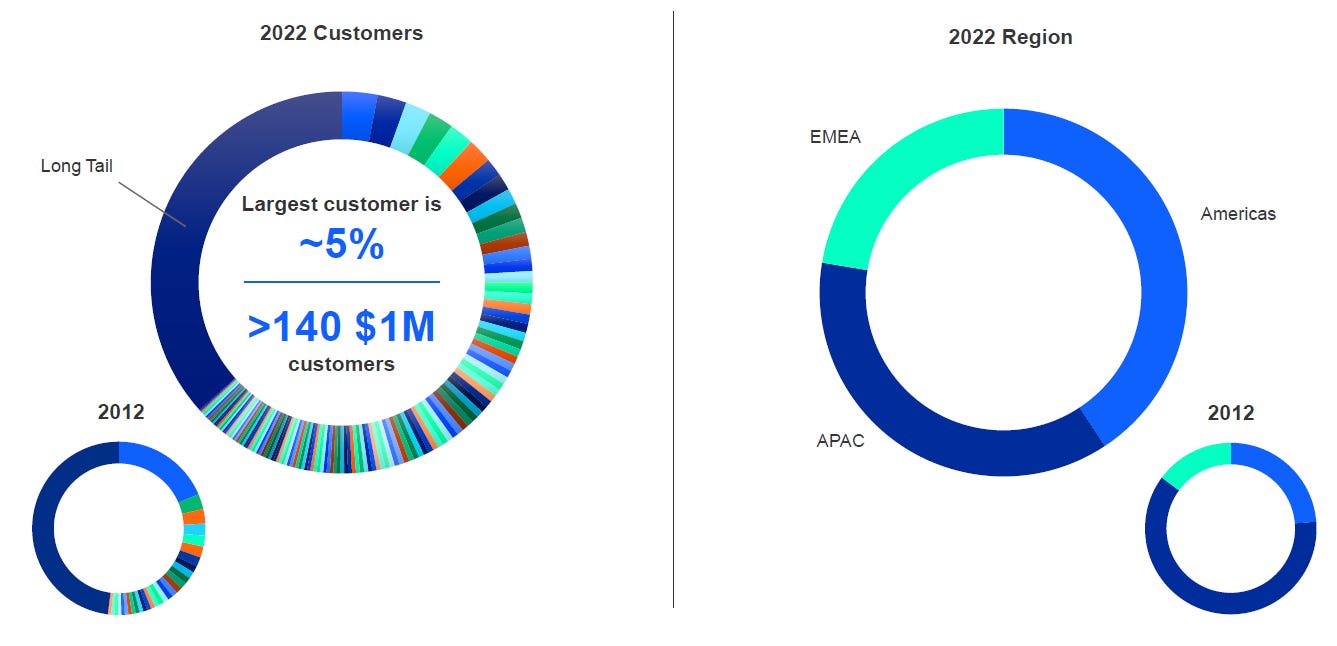

The other attraction is that SiLabs has a very diversified customer base:

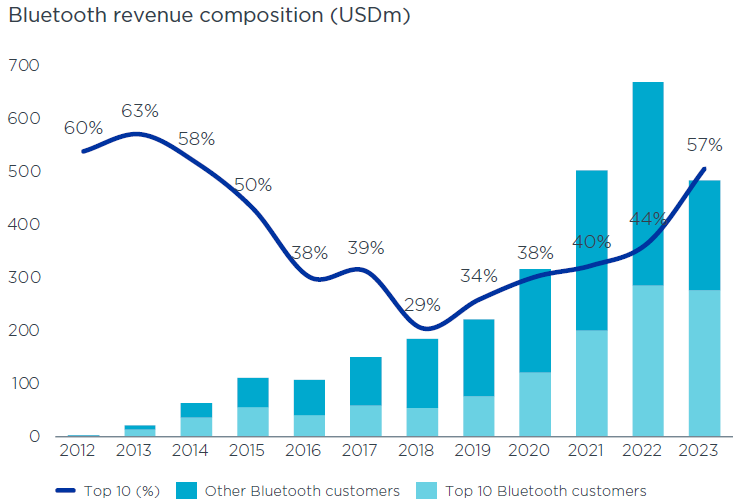

Whereas Nordic is more concentrated with 10 customers making up 57% of their core Bluetooth revenues:

So both are fairly interesting names and the risk-reward should be reasonably attractive for investors in the space. The industry has fairly high barriers to entry combined with an attractive growth profile, but in terms of volumes as well as on the ASP side with SoCs becoming ever more advanced. Lastly, growth rates should exhibit a strong recovery once we leave the current downturn as can be witnessed in SiLabs’ very strong pipeline.

If you enjoy research like this, hit the like & restack buttons, and subscribe if you haven’t done so yet. Also, please share a link to this post on social media or with others who might be interested, it will help the newsletter to grow, which is a good incentive to publish more.

I’m also regularly discussing tech and investments on my Twitter.

Disclaimer - This article is not a recommendation to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it can not be guaranteed that all information used is of this nature. Before making any investment, it is recommended to do your own due diligence.