Klaviyo, a bigger opportunity than Hubspot in '16?

Klaviyo, a bigger opportunity than Hubspot in '16?

A software play on the growth in e-commerce

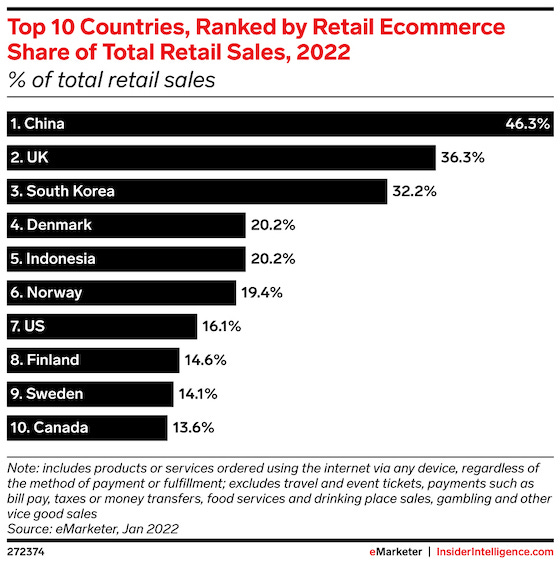

E-commerce remains an interesting area for investment exposure as penetration rates around the world still leave a lot of room for growth. Even in the top 10 countries by penetration rates, e-commerce is still only taking up around 15 to 35 percent of retail sales, which means that plenty of countries will still have penetration rates of below 15%:

Consequently, a variety of e-commerce names should be able to generate double-digit top line growth rates for some time to come:

Software businesses are usually attractive for investors: revenues tend to be sticky, giving scope for price increases over time, while bringing in recurring and largely non-cyclical cash-flows. These characteristics have turned many of the good quality software names into attractive compounders over the last decades.

One feature that attracted me to Klaviyo’s software is that their pricing is based on the volumes of data that run over their platform. Thus, small mom-and-pop e-commerce merchants — typically operating over Shopify — will face little cost initially for bringing their data into Klaviyo. This gives them the opportunity to grow their businesses with low initial investments, which then over time brings in revenue growth for Klaviyo as their customers’ businesses grow. So the software is not sold on a per seat basis like you have a with a lot of other subscription models, e.g. $24k per annum for a Bloomberg terminal.

Klaviyo is a marketing automation platform for e-commerce merchants, although they are now planning to move into other verticals as well. The platform allows you to automate and customize your email, SMS, and push notification campaigns as a merchant. So not really the most exciting business in terms of advanced technology, like say an ASML or TSMC, it’s a typical boring piece of business software. However, there is a potential data advantage here. As with the use of AI, Klaviyo’s platform can learn which types of campaigns tend to work better in terms of sales conversions and then bring these suggestions to the merchants.

The company mentioned on the Q3 call that they already have 135,000 customers, and that their platform generated $37 billion in additional revenues for their customers. This would mean that the average customer generated around $280,000 of sales over the Klaviyo platform, with the company obtaining a take rate of 1.3% as reflected in their $473 million of annual revenues.

As the company was only founded in 2012, clearly growth has been strong, and on the last quarterly results top line growth remained close to 50%:

An example of Klaviyo’s dashboard and of an email campaign you could automatically send out to users, in this case to those who left items in their shopping basket:

You could similarly target previously loyal customers who now haven’t returned to the store over the last three months, so you could try to bring them back with an attractive 25% discount on their next shopping basket for example. Klaviyo’s strength is that you can really segment customers in loads of ways and then create specific campaigns to appeal to these groups. With the use of LLMs, we’re probably moving towards a world where every email could be customized for a particular customer. Also other AI features such as making new product suggestions based on past purchases are usually good at converting into sales.

Klaviyo detailing their platform in the prospectus, as well as the disadvantages of legacy solutions:

“Other software solutions were not purpose-built to harness customers’ first-party data to deliver impactful consumer experiences. Data-focused offerings, such as cloud data warehouses or operational databases, provide the ability to store and analyze significant volumes of data for general-purpose use cases but are not purpose-built for consumer data and lack the front-end application layer. Marketing solutions are insufficient because they lack the underlying data intelligence. Simple marketing solutions use a flattened and narrowed view of a consumer’s historical data. This basic profile data alone significantly limits the granularity of segmentation businesses can use. Profile data is also difficult to combine with event data, which includes all digital touch points of a consumer’s engagement with a brand and provides necessary real-time information.

In an attempt to bridge this gap, other marketing solutions use a patchwork of third-party technologies, such as separate consumer data, learning, and messaging applications. These solutions often require significant technical expertise to implement, operate, and maintain, which limits flexibility, reduces speed, and increases costs. Furthermore, these solutions are not able to provide clear revenue attribution, minimizing ROI.

By vertically integrating our data layer and marketing application, we make it easy for businesses to create and store unified consumer profiles and then use those profiles to derive new insights and ultimately drive revenue generation. We purpose-built a centralized, scalable, and flexible cloud-native data store for our customers to intelligently aggregate and process first-party consumer profile and event data without friction. This approach enables our customers to seamlessly generate unified and highly-granular consumer profiles, populated with data from customers’ systems and from over 300 third-party integrations, from eCommerce platforms – such as Shopify, Salesforce Commerce Cloud, and WooCommerce – to loyalty, customer service, and shipping solutions.

We built an application layer on top of our data layer to provide a comprehensive set of tools and features that enable our customers to easily turn consumer preferences into insights and actions. Combining our data layer and application layer into one vertically-integrated platform allows our customers to rapidly segment their consumers, easily create highly-personalized experiences, and automatically send messages customized to their unique brands.

Our platform and customers benefit from significant network effects. We assembled over 6.9 billion consumer profiles across our customer base, and in the twelve month period ended June 30, 2023, we processed over 695 billion events, which are data on how consumers engage across channels, such as opening an email, browsing a website, or placing an order. As we add more customers and more anonymized data on our platform, we are able to better refine our predictive models of consumer behavior.

Our platform offers simple, one-click drag-and-drop customizable templates for designing messages and generative artificial intelligence tools for creating content. For advanced functionality, we offer a suite of tools to enable developers to build rapid automations for different use cases and quickly integrate with other systems efficiently. Our platform also allows our customers to compare their performance against similar companies in their respective industries and makes recommendations on how to optimize future engagements.

We are maniacally focused on making our platform intuitive and exceptionally easy-to-deploy, driving our customers to expand their usage of our platform in a self-serve manner.”

Take what they said about competitors with a grain of salt, there are a number of competitors with good products as we’ll see below. However, the point they made on data being a competitive advantage is an interesting one, as this would make it hard for new entrants in the field to start competing. So this would mean that the players with the largest amounts of data would be able to provide better AI algorithms to drive better returns for clients. So cost of the platform would then become a secondary factor, if you can generate 10% higher revenues with Klaviyo, you don’t really care whether the competitors’ take rate is say 0.5% versus Klaviyo’s 1.3%.

Transformer-based AI models are also making Klaviyo’s platform more accessible for users. The CEO gave an example on the earnings call of how an advanced query can be designed based on common text, so there’s no need for the user to learn a database querying language:

“We continue to add more artificial intelligence features to our platform. During the quarter, we started to roll out a new natural language interface for our segmentation builder. This allows customers to define queries into their data without specific knowledge of the underlying data structure. We believe these kinds of features increase the accessibility of our software and the number of experiments a business can run.”

This certainly sounds like it would make the platform much more effective and as a result boost usage, and we’re only at the start now of LLMs really. So this could accelerate growth in the coming years.

Klaviyo’s platform is integrated with third-party e-commerce platforms such as Shopify, Salesforce commerce, and Woocommerce. The company mentioned 300 such integrations in their prospectus. On top of that, Shopify made a $100 million investment in Klaviyo two years ago. Here is Shopify’s President discussing the Klaviyo IPO on their Q3 call:

“On the app side, our long-term partner Klaviyo, who officially launched their app in the Shopify App Store back in 2018, has successfully IPOd, which demonstrates the strength of Shopify's ecosystem in helping our partners find success. Congratulations to the entire Klaviyo team on this huge achievement.”

As already mentioned, the pricing model is one of the attractive features of this platform. Klaviyo explained in their prospectus how revenues grow with the amount of data processed:

“Our subscription plans are tiered based on the number of active consumer profiles stored on our platform combined with the number of emails and SMS messages sent. As our customers’ businesses grow, they utilize more consumer profiles and send more emails and SMS messages, which naturally increases their usage of our platform. Our revenue also expands when our customers add additional channels, such as SMS, or when their other brands, business units, and geographies start using the platform.

In addition, we recently launched our reviews and Customer Data Platform (CDP) products. Klaviyo reviews allows customers to collect product reviews alongside consumer data and messages. Klaviyo CDP gives customers user-friendly ways to transform and cleanse data, run more advanced reporting and predictive analysis to drive revenue growth, and sync data into and out of Klaviyo at scale. The success of our land-and-expand strategy is evidenced by our highly-attractive NRR.

When we first launched our platform, we intentionally focused on serving entrepreneurs and small and medium-sized businesses (SMBs). As our customers have scaled and become mid-market companies and larger enterprises themselves, their success with Klaviyo has attracted more interest from similarly sized businesses that are looking to drive better engagement with their consumers. As such, we have continued to build out a sales team to focus on mid-market and enterprise customers.”

For the last few years, NRRs have been at 119% for Klaviyo, which basically means that existing customers are spending 19% more per annum on the platform than in the prior year.

The CEO explained on the earnings call how the data from the new reviews product can be leveraged for their customers to create better and more customized campaigns:

“Reviews are an opportunity for a business to learn more about their consumers and then use that data. So what’s really great is you can use Klaviyo’s marketing software platform to then collect reviews. And then that review data can be used to personalize marketing. So there’s this kind of viral loop that’s there.”

We also got an update how the company is growing larger accounts on the call:

“At the end of the third quarter, we had almost 1,700 customers generating ARR of over $50,000 per year, which was up 89% year-over-year. This growth has been fueled by both expanding use of our platform by our customers and landing new, larger accounts. We are seeing customers consolidate more of their marketing software spend onto Klaviyo, with some of our largest customers [spending] over $0.5 million in ARR.”

Given that a lot of customers are small mom-and-pop merchants, new customers typically arrive via the self-service channel. Klaviyo mentioned a CAC payback period of only 14 months in the prospectus. Starting up on the platform seems fairly easy for new customers, this is again taken from the prospectus:

“Once customers access the Klaviyo platform, they can easily integrate with more than 300 critical third-party data sources to import and explore their first-party data and design and run campaigns and automations, providing rapid time-to-value.”

Doing some background checks on the product, for example by looking at some Youtube videos made by users and e-marketers, the overall tone was that for e-commerce, Klaviyo is a no-brainer, although that for other verticals, competitors such as MailChimp can be better suited.

Similarly on Software Reviews and G2.com, Klaviyo’s platform is among the best rated solutions:

These are the pros and cons of Klaviyo mentioned on G2.com’s reviews — clearly integrations, user friendliness, and user interface are the net positives. While price tag and slowness are potential detractors. If you need to send out thousands of emails, obviously this will create some waiting times.. Reading reviews, users especially like the ability to segment customers.

Klaviyo discussed the opportunity to enter new verticals in the prospectus:

“While our first use cases were focused on the retail and eCommerce vertical, we believe our platform is highly extensible across a broad range of verticals, including education, events, entertainment, restaurants, travel, as well as B2B companies. As we continue to scale our platform, we expect that our total addressable market will expand to businesses in all verticals that engage with third parties. Accordingly, we estimate that the total addressable market opportunity for our platform across all of these verticals is $34 billion in the United States alone. We believe our opportunity outside of the United States is at least as large as our domestic opportunity, implying a total global addressable market of $68 billion.”

Finally, there is the opportunity to expand further internationally, as revenues from the US are currently contributing 70% to revenues.

Hubspot comparison

Klaviyo reminds me a lot of Hubspot when I first looked at in 2016. Hubspot is a CRM software for SMBs and has been a phenomenal story. The share price has gone up more than tenfold, driven by extremely solid revenue growth:

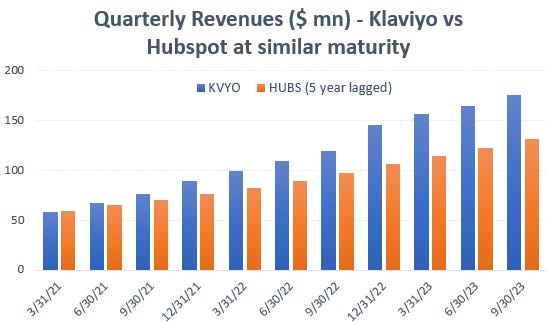

However, plotting Klaviyo vs Hubspot at similar stages of maturity, we can actually see that Klaviyo is growing even faster:

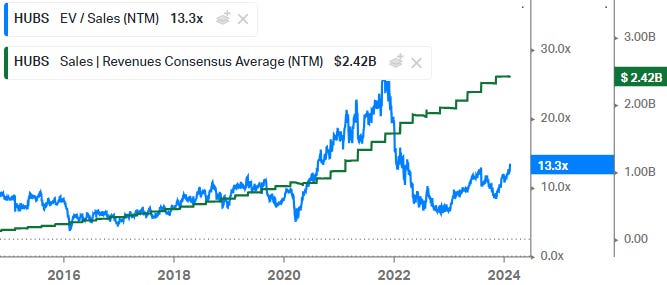

Hubspot used to trade around 8x forward Sales at that time (the blue line below), similar as Klaviyo now. Note that even despite Hubspot becoming a much larger company, the multiple has only go up. Usually it is the other way around, with high-growth stocks coming to market at high multiples, and then over time these companies grow into their multiple, a process called de-rating. Clearly in ‘16, the market was dramatically underestimating this business.

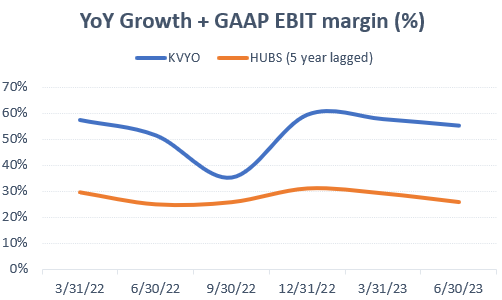

Also if we take into account how much these companies are burning cash to generate their growth, Klaviyo is scoring much better on this metric. If we simply add up YoY growth rates and EBIT margins (GAAP, taking into account SBC), we can see that Klaviyo has been hovering around 55% growth + margins, while Hubspot only managed to generate around 25-30%. Although SBC tends to go up post IPO, so this helps Klaviyo here as the company was still private on this analysis:

So, Klaviyo is growing faster, showing a much better profitability profile, but is trading on a similar multiple as Hubspot when it was at similar stages of maturity. We know that Hubspot’s share price subsequently went all the way. So this should provide an attractive opportunity set for Klaviyo’s shares, we’ll do more work on the valuation below.

Fears around email changes

There have been some fears in the market around the new email policies both Gmail and Yahoo will introduce as from this month. These are targeted at bulk senders, i.e. those sending more than 5,000 emails per day. It’s all about reducing spam in inboxes, so senders need to have a one click unsubscribe button and need to be authenticated for example.

So intuitively, it shouldn’t make much difference as Klaviyo’s emails have these features already. However, I also had a discussion with Google’s new LLM Gemini on this, as he might have some good insights on Google’s policies, and Gemini thinks it will actually help Klaviyo:

“These changes generally favor good email marketing practices, which Klaviyo already encourages. Implementing strong authentication (SPF, DKIM), offering easy unsubscribe options, and maintaining good email hygiene are core Klaviyo principles. So, for most users, these changes shouldn't be disruptive, and may even improve deliverability rates over time.”

Also Goldman thinks these fears are overdone, from the fly:

“Goldman Sachs upgraded Klaviyo to Buy from Neutral with an unchanged price target of $36, which represents 30% upside. The analyst sees the stock's 22% underperformance over the last three months versus the Nasdaq 100 as a buying opportunity. Concerns around a disruption to Klaviyo's business model from ongoing changes to email spam filtering are overdone based on recent industry conversations, the analyst tells investors in a research note. The firm expects to see continued evidence of ‘share gain up market given Klaviyo's differentiated approach’ to the software infrastructure underpinning its marketing application.”

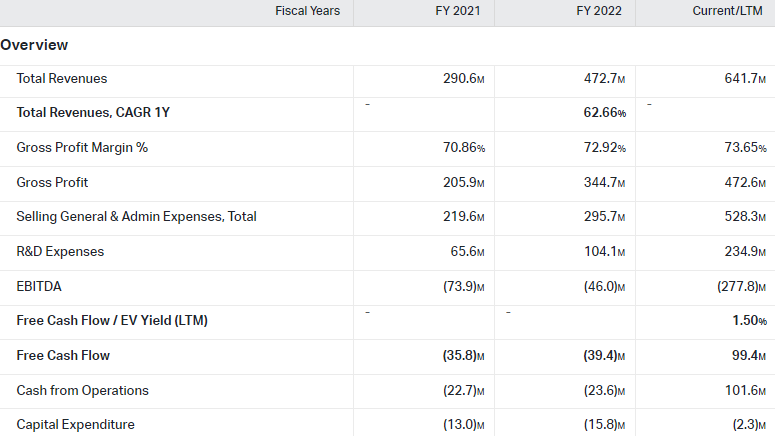

Financials — share price of $28.2 on the NYSE at time of writing, ticker KVYO

Sell side analysts are modelling in reasonably conservative top line growth estimates for ‘24 and ‘25 of around 27-28% per annum. While over the last quarters, the company has been growing at a rate of around 50%. Management did mention that they put in a price increase during Q3 of ‘22, so this will have boosted growth rates over the last year, although it looks like the business was generating similarly high growth rates beforehand as well. And the effects of this were already waning in Q3 of ‘23. Valuation at 8x forward sales looks very reasonable for a high growth story like this:

You can also see above that the business has around $700 million in cash on the balance sheet, while turning free cash flow positive in the cash-flow statement over the last twelve months (statements below). So there shouldn’t be any risk of an additional capital raise being needed, while the company can actually start deploying cash to offset SBC dilution. The CFO guided for normalized SBC post the IPO of around $40 million in Q4, so annualizing this number would result in around $160 million per annum. However, going forward with the progress the business is making, free cash generation should become sufficient to offset these with share buybacks.

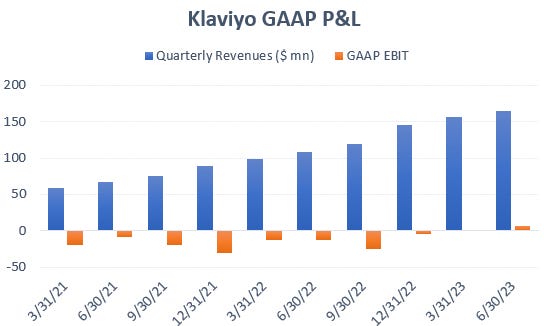

You can see above that EBITDA over the last twelve months dropped due to the high SBC from the IPO. However, pre-IPO, the business already managed to turn profitable on a GAAP basis, and I suspect due to continued growth and a normalization of SBC, in the coming years it should again be able to return to GAAP profitability:

The above chart also shows that Q4 tends to be the highest growth quarter due to the shopping season.

Compared to peers, Klaviyo is expected to generate the highest top line growth rates, while trading on lower EV to Sales valuation:

Overall, this should be a fairly decent business. It’s not super high quality, but it’s a typical piece of business software that’s clearly addressing a need in the market and that’s executing well. The runway for growth could well be long, potentially even better than Hubspot, and currently you’re not paying that high a multiple for it. Good software companies can easily trade around 4 to 8x forward sales when reaching fairly mature levels of growth, so paying 8x for a company which is still in hyper growth mode, and which has managed to reach GAAP profitability, is close to the best risk-reward one can come across investing in business software. The main risk is that growth would start stalling somewhere in the coming years, and then the company would have to start showing that it can work itself to a high EBIT margin instead. If it manages to do that, the valuation still would make sense.

If you enjoy research like this, hit the like and restack buttons, and subscribe if you haven’t done so yet. Also, please share a link to this post on social media or with others who might be interested, it will help the publication to grow.

I’m also regularly discussing tech and investments on my Twitter.

Disclaimer - This article is not a recommendation to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it can not be guaranteed that all information used is of this nature. The views expressed in this article may change over time without giving notice. The future performance of the mentioned securities remains uncertain, with both upside as well as downside scenarios possible.