Applovin, deep value adtech to double again?

Applovin, deep value adtech to double again?

Long thesis

A bird’s-eye overview of the adtech ecosystem

Adtech can be an obscure field, due to the wide variety of types of players involved. However, obviously it can be a lucrative field for investing as dominant social media players active in the field such as Google and Facebook are printing cash, while also pure-play strongly positioned players such as The Trade Desk have been excellent performers.

In a nutshell, in adtech advertisers are aiming to reach consumers via digital ads, such as in the Wall Street Journal or on Instagram, and there a variety of ways of linking these two parties. Traditionally, an advertiser would hire an agency which would have deals in place with publishers such as the WSJ to buy advertising space, but with the rise of the internet in the digital world this has mostly moved towards programmatic buying. So when a visitor on the WSJ app starts reading a news story, the WSJ will let potential buyers know that there is an ad space available. Available ad inventory is aggregated on supply side platforms (SSPs), which in turn provide this supply to ad exchanges as available for sale. Advertisers in turn make marketing budgets available on demand side platforms (DSPs) such as The Trade Desk, which place bids for available inventory on exchanges.

DSPs and SSPs can also connect to ad networks to buy and sell ads, the best known networks are Google and Facebook, although they can also operates an ad exchange. Ad networks are more of a vertically integrated solution for the ad supply chain, while ad exchanges purely match supply and demand. Typically large advertisers and publishers go mostly over exchange, whereas smaller players go mostly over the networks due to the more complete and more user friendly offering. The above illustration shows how an advertiser like Coca Cola can have its ad displayed on a digital property over multiple avenues.

An overview of Applovin

The interesting feat about Applovin is that it is an adtech software business focused around mobile gaming, which is a $90 billion market expected to grow at a 7% annual rate (chart below). This market was strongly impacted by Apple’s ATT (app tracking transparency) policy, which requires apps to request permission from users before tracking their data across apps or websites. Traditionally, users could be automatically tracked via an anonymous identifier (a unique and randomly generated ID based on your device), which gave advertisers insights into the interests of this particular consumer. As most consumers subsequently opted out, this brought a large correction in the value of the mobile ad market during ‘22, as well as with lockdown policies unwinding.

However, this damage is now done and so we should be able to move forward from here. And even though Google will likely face out cookies in the coming years to replace them with a fully anonymous profile (a vector indicating the set of interests of any user), as Google makes almost all its money from ads, one can be reasonably sure that this won’t work any worse than the cookie mechanism (and maybe even better). Employee stock options tend to align shareholder and employee interests extremely well.

Applovin’s CEO discussing the risk of privacy changes on the recent call: “Look, we’ve dealt with privacy changes probably since 2014. Every time there’s a change on platform or with regulators, you’ve changed something in your stock rating, but we’re a nimble company. We’ve rewritten our core technology multiple times over the years and perform in the face of any of those kinds of changes.”

The mobile gaming market is really divided into two parts, one is in-app purchases, which is around 80% of the market, and the other is advertising, which is used mostly in casual games and is the area where Applovin is mostly operating. Puzzle-type games are a big category here, things like Candy Crush. It’s actually the in-app purchases market which got hardest hit by Apple’s changes as it became much harder to target new players who spend money in games. Despite this hit to the market, Applovin’s software platforms continued to grow well, more on this below.

Applovin has a software platform which consists of two modules focused around mobile gaming adtech. One is its mediation software, Max, which allows a game publisher to connect to a wide variety of ad networks and exchanges, ensuring that its ad inventory can be sold to the highest bidder. This in turn generates a lot of useful data for Applovin, as they know which gamers are interacting with ads, which can then be leveraged for their app discovery platform, powered by their Axon AI engine. The hard thing for a game publisher is to make potentially interested gamers aware of their newly released game. So this is where app discovery comes in, this software can place ads for your games inside other games, and Applovin makes money here on the spread between what it has to pay to acquire ad inventory, and the revenues it generates from its clients.

So whereas the first ad mediation platform (Max) is a traditional take rate business model, where Applovin takes a 20% cut on the revenues a publisher is making from selling game ads, the app discovery business (Axon) is more like a trading business, where Applovin has been paid to generate a certain amount of traffic or revenues to its clients, and has to acquire a certain amount of ad inventory to achieve this. The second is obviously not the highest quality business, it reminds me somewhat of Criteo, but I suspect that Applovin can leverage from the data they’re generating in their ad mediation platform. So they could have a reasonably sustainable competitive advantage here, especially as they have a large market share in these markets and as the traditional ad networks such as Meta and Google can’t track a lot of users anymore on Apple devices, making their visibility and historical data advantage much more limited. Applovin’s CEO mentioned that 50% of gamers are not allowing to share their data for personalized advertising.

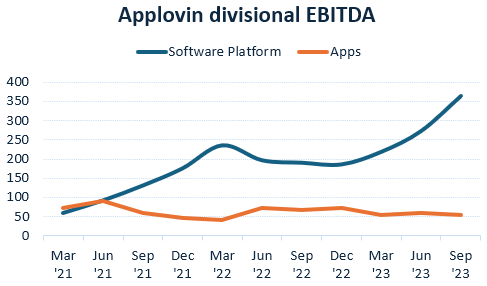

The company also still has a gaming business, which was originally cobbled together by acquisition both to gather data as well as to showcase how they’re able to grow the user bases of these games with their discovery platform. Currently this business consists of around 350 games from 11 studios. However, as the company’s software platforms have been successfully scaling up, gaming has become a small contributor to EBITDA (chart below). Also, due to this growth in the software platform, by far most of the data is now acquired from third party games, so that currently there isn’t really a need anymore to feed proprietary data into their AI engine. As such, the gaming business is up for sale and if the right offer comes, it will likely be gone. Alternatively, this business will be ran for cash which is being returned to shareholders.

Mobile gaming is a very competitive market so as this business has now become a small contributor, this should be attractive for shareholders as it mitigates the competitive risk intrinsic to this business. The software platform is the real attraction within Applovin due to the much less competitive nature. The key competitor here is IronSource which is now merging with Unity. Although IronSource is the smaller player, Unity is a fairly dominant engine to develop mobile games, so it is possible that IronSource can leverage here from Unity’s client base and platform to gain share. Applovin’s advantages are that software tends to be a sticky business and that they should have a data advantage due to their larger scale.

Applovin’s CEO discussed the competitive environment at the JP Morgan conference last year: “Max has already grown to become the largest in the sector in terms of publisher adoption. The only other three solutions to service publishers at scale were MoPub, IronSource and Google. By bringing in MoPub, then number two, we put the majority of the inventory on one platform. We sit on top of 700 million daily devices that are playing games being monetized by the Max platform. So it’s a substantial audience and it gives us a good opportunity for growth in the future. Also having the control of the ecosystem across our technology stack is a material advantage because we’ve got the marketplace (app discovery) and two-thirds of the ad ecosystem flowing through our technologies (Max), so we’ve got a lot of visibility to understand exactly what’s coming.”

Clearly, if the user base is 700 million daily devices, this should put Applovin in a strong position. So the two-thirds i.e. 66% market share could make sense. MoPub is an ad mediation platform which Applovin acquired from Twitter and where they managed to move the client base over to Applovin’s platform within 90 days. Clearly very impressive and well executed.

The CEO highlighted other synergies between the two software businesses at the same conference: “What’s interesting about our advertising business is that the vast majority of our advertising dollars on the app discovery side come from our Max publishers. We end up their largest partner, both on the monetization side and the growth side. Now that we have two-thirds roughly of the in-app ad ecosystem on our platform, it creates this strong closed loop, where our most important customers are app developers. They’re performance buyers, buying on app discovery. Our customers might end up being even a five person development shop out of Turkey that spends money on our platform on a performance and arbitrage basis. These types of companies will spend $1 to make $2 all day long in any economy.”

discussed Applovin’s competitive position with : “IronSource just doesn’t have the plug-in to the Google Network at all, actually. So, if you’re bidding on the Google demand side for mobile games, your bids will just not go through to IronSource. Right now, they’re mostly done with AppLovin.”As a result of these factors, Applovin’s software business has been able to generate stellar growth (chart below) — note however that it doesn’t strip out the early ‘22 MoPub acquisition, although growth clearly remained strong over ‘23:

The CEO mentioned that they have over 500 large enterprise clients who generate the majority of revenues, so the client base is very diversified, indicating the highly competitive nature of mobile gaming. While the net dollar retention rate is over 200%, meaning that existing clients spent more than twice as much on Applovin’s software compared to the previous year.

Financials - share price of $41 at time of writing, ticker APP on the Nasdaq

The underlying software business has been going like a train which has been offset by a cyclical decline in the apps (gaming) business. Last quarter, the software business grew 65% year over year driven by a new release of their Axon AI engine while also for the first time in years, the gaming business returned to sequential growth:

While the software business is now contributing 87% to overall EBITDA:

So essentially, the best way to look at Applovin is to really see it as the software platform business, as the contribution from gaming apps has become very small and this business should be disposed off anyways at some stage.

Applovin’s CEO discussing the roll-out of their new AI engine on the last call: “Axon 2 was rolled out partially in the prior quarter. This is a brand-new technology, and it’s a self-learning type of technology. These AI models as they get scaled, continuously improve themselves. And then our team also is able to continuously improve them. So we’re talking about a new technology that’s been game changing for our business and is in the first inning.”

They’re also rolling out Axon 2 to connected TV (CTV, i.e. streaming apps), which is an opportunity also the Trade Desk has been talking a lot about. While I haven’t spent time on this business in this note as it is still negligible, it is basically a free call option embedded in the share price if they do succeed here. Similarly, they’re also growing in non-gaming apps, so their addressable market is clearly expanding. The company’s CEO discussing these two on the latest call:

“Obviously, it’s television, and we all also know that performance marketing on TV hasn’t really been anywhere near as much as it has been on desktop or on mobile devices. And so our technology is truly cutting-edge and being able to extend into that platform presents a very big opportunity. And then Array is the same deal, this gets us on Android devices today in a much more intimate way. It presents multiple new ad offerings to the consumer and being able to use the Axon 2 solution there. We think this is also going to be game changing for that business. Non-gaming is growing faster because it is materially smaller, it will take a sales effort to substantially grow so that it can become a much more material part of the business. But the technology works very effectively regardless of the type of app.”

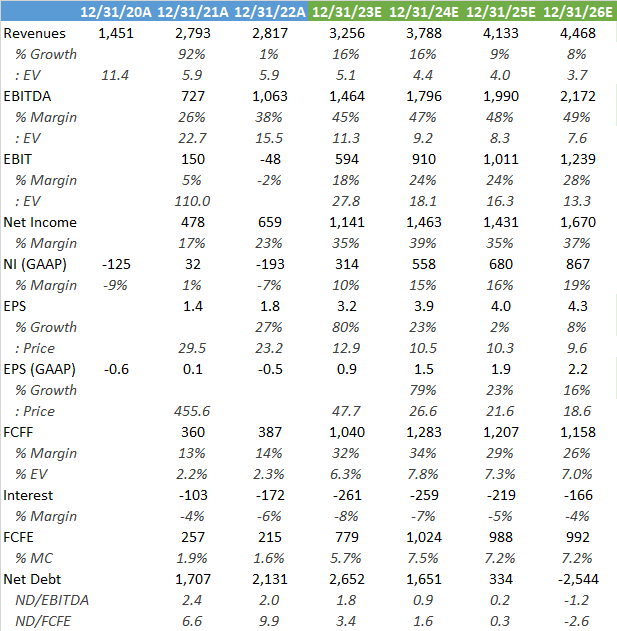

The company is guiding to do USD 430 million of EBITDA in Q4, which would give an annual run rate of USD 1.7 billion, making the stock trade on only 9x EBITDA. The sell side’s numbers look very low as they’re only modelling in USD 1.8 billion in EBITDA for ‘24. This is likely to reach over USD 2 billion.

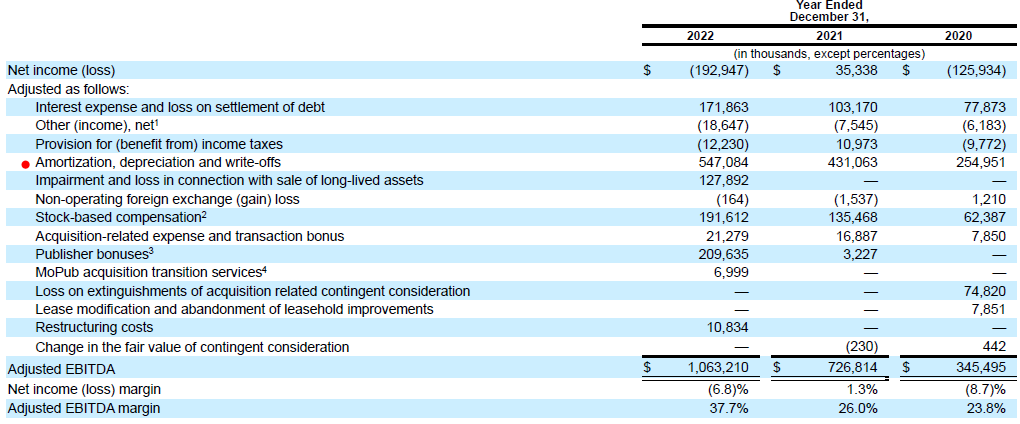

However, on a GAAP basis, we’re looking at 27x next year’s earnings. The annual report shows that this difference in adjusted and GAAP numbers is being driven by depreciation and write-offs of non-tangible acquired assets. Basically they’ve been already optimizing their portfolio of gaming studios, something which

pointed out to me. So over time this should unwind and then we will get the GAAP margin uplift as well..

Stock based compensation (SBC) has been steadily on the rise and we’re looking at USD 323 million already over the last 12 months. However, the company is offsetting the dilution from these with share buybacks, something they can easily do as the FCF is much larger. They mentioned on the last call for example that they had already been buying back USD 1.2 billion of stock year to date.

On the face of it, this is not a bad business and which is actually generating high EPS growth while trading on a low valuation. If they can keep generating solid EPS growth combined with some re-rating, this is a name I could see doubling again — the stock has already doubled twice over the last year:

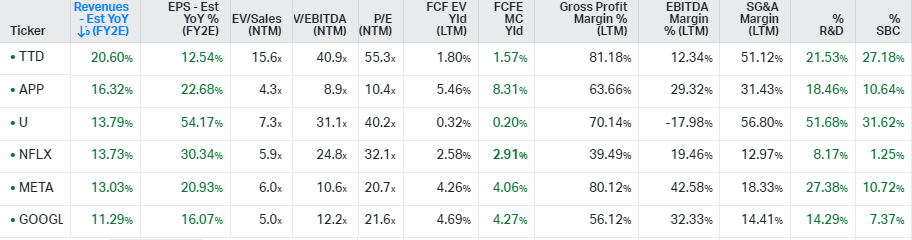

All the other stocks in the peer sheet below are in my opinion higher quality so they deserve to trade on a higher multiple. But I could easily see Applovin re-rating to 15-18x EPS or so as the market grows more comfortable with the sustainability of its software business. Combining that with future EPS of potentially USD 4.5 and share buybacks, investors in this name could make a 100% return over time, this is if the company keeps executing well. Note that I do think this is a higher risk name, so it’s not a stock I would hold a large weighting in.

If you enjoy research like this, hit the like button and subscribe. Also, please share a link to this post on social media or with colleagues with a positive comment, it will help the publication to grow. All shares are appreciated.

I’m also regularly discussing tech and investments on my Twitter.

Disclaimer - This article is not a recommendation to buy or sell the mentioned securities, it is purely for informational purposes. While I’ve aimed to use accurate and reliable information in writing this, it can not be guaranteed that all information used is of this nature. The views expressed in this article may change over time without giving notice. The future performance of the mentioned securities remains uncertain, with both upside as well as downside scenarios possible. Before investing, I recommend speaking to a financial advisor who can take into account your personal risk profile.

Always been intrigued by app. Issue has been hard to understand biz. Software side actually seems like wrong name for the biz. Doesn’t seem to be accurate description for it to me. Great article.

Thanks for the idea and nice write-up. Outside of consensus ests maybe being too low and the company trading at ~26x '24 Adj. EPS / ~21x '25 Adj. EPS vs TTD trading at +50x, what (if any) do you see as the main catalysts here? Any spinoff of gaming, increased buyback, M&A, or corporate action probable over the next 24 months?